Observations:

• Out of about 320 focused sustainable long-term mutual funds and ETFs totaling $381.9 billion in assets as of January 31, 2026, only 27, or less than 1%, with $18.1 billion in assets include “impact” in their names to indicate a sustainable investing impact-oriented approach.

• This small segment of funds is dominated by taxable and municipal bond funds, a total of nine funds/29 share classes, with almost $14 billion in net assts. The rest consist of US and international equity funds. In total, 16 fund firms offer these funds, but the group is dominated by Nuveen, Community Capital, Domini and Praxis Investment Management, which together account for 84% of assets.

• Across academia, asset owners, regulators, and industry bodies, a widely accepted and de facto industry standard of “impact” and “impact investing” comes from the Global Impact Investing Network (GIIN). According to GIIN, impact investments are investments made with the intention to generate positive, measurable social and/or environmental impact alongside a financial return. This definition has three required elements: (1) Intentionality–impact is an explicit investment objective, (2) Measurability–impact outcomes are identified and assessed and (3) Financial return–investments are expected to generate a return (not philanthropy).

• That said, the approach that characterizes the 27 funds with the term “impact” in their names can vary significantly. These approaches span from impact investing aligned with GIIN’s rigorous definition that integrates intent plus measurement as well as reporting, to a strong impact-aligned strategy, to a thematic or impact-aligned investing, to an impact-branded ESG/values investing that focuses on values alignment but with limited accountability.

• That being the case, sustainable investors and financial intermediaries seeking exposure to impact-oriented public investments in the form of mutual funds and ETFs should reflect on these variations when considering their impact investing options.

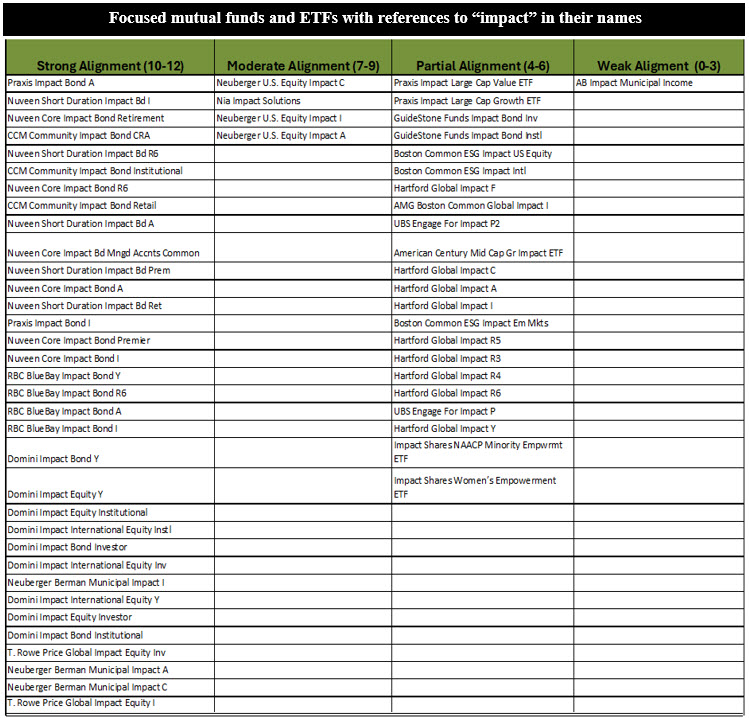

• The chart above classifies the 27 funds and their respective share classes, in the case of mutual funds, into one of four categories based on an evaluation of each fund across the four independent dimensions that reflect the widely accepted GIIN definition of impact investing, including intentionality, contribution, measurement as well as accountability and reporting. Each dimension has been scored on a 0–3 scale, for a maximum total score of 12. Funds achieving a score between 10-12 are considered to reflect a strong alignment with the GIIN definition (10 funds in total), funds achieving a score between 7-9 are considered to reflect a moderate alignment (3 funds in total), funds achieving a score between 4-6 are considered to reflect a partial alignment (13 funds in total) and funds achieving a score between 0-3 are considered to reflect a weak alignment with the GIIN definition (1 fund).

Notes of Explanation: The universe of 27 funds have been scored based on four key characteristics that are considered within the widely accepted and de facto industry standard of “impact” and “impact investing” developed by the Global Impact Investing Network (GIIN), including (1) Intentionality-impact is a stated objective, (2) Contribution-capital plausibly enables the outcome, (3) Measurement-outcomes are tracked and disclosed, and (4) Accountability and Reporting-impact reporting and stewardship. Each dimension has been scored on a 0–3 scale, for a maximum total score of 12. Funds achieving a score between 10-12 are considered to reflect a strong alignment with the GIIN definition, funds achieving a score between 7-9 are considered to reflect a moderate alignment, funds achieving a score between 4-6 are considered to reflect a partial alignment and funds achieving a score between 0-3 are considered to reflect a weak alignment with the GIIN definition. Funds data sources, Morningstar. Otherwise, Sustainable Research and Analysis LLC.

Notes of Explanation: The universe of 27 funds have been scored based on four key characteristics that are considered within the widely accepted and de facto industry standard of “impact” and “impact investing” developed by the Global Impact Investing Network (GIIN), including (1) Intentionality-impact is a stated objective, (2) Contribution-capital plausibly enables the outcome, (3) Measurement-outcomes are tracked and disclosed, and (4) Accountability and Reporting-impact reporting and stewardship. Each dimension has been scored on a 0–3 scale, for a maximum total score of 12. Funds achieving a score between 10-12 are considered to reflect a strong alignment with the GIIN definition, funds achieving a score between 7-9 are considered to reflect a moderate alignment, funds achieving a score between 4-6 are considered to reflect a partial alignment and funds achieving a score between 0-3 are considered to reflect a weak alignment with the GIIN definition. Funds data sources, Morningstar. Otherwise, Sustainable Research and Analysis LLC.