Introduction and Summary Conclusion

An article published in the July 13, 2017 issue of Bloomberg’s Sustainable Finance entitled “These 10 Funds Have A Conscious…and Perform Spectacularly” promoted the idea that “investing for good can also be a good investment” based on the fact that “a number of mutual funds that take environmental, social and corporate governance (ESG) factors into account when making investment decisions have proven to be stellar performers.”

The article went on to report that two of the top 10 funds beat the S&P 500 Index by wide margins during the one-year period ended June 30, 2017 as did two other funds. While the margins of outperformance were more limited, these two funds also exceeded the performance of the S&P 500 over the 3 and 5-year intervals. That was generally not the case for the other funds. While it is true that the two top performing funds, the Parnassus Endeavor Fund and the Parnassus Fund, both delivered outstanding aggregate results over the preceding 1, 3, 5 and even 10 year time intervals, the performance track record achieved by the group of 10 funds as a whole is less inspiring based on a more carefully constructed examination of the funds, their investment objectives and strategies as well as their performance relative to appropriately selected securities market indexes. In fact, the results show that, excepting for the latest 1-year period to June 30, the same 10 funds managed to outperform their benchmarks only between 34% and 41% of the time. While this record of achievement surpasses the results registered by domestic equity funds more generally (i.e. equity funds without ESG as a general attribute), it’s still below average. This conclusion is in line with the theme recently set out in an article published by Mark Hulbert in MarketWatch[1] that while there are many reasons to take environmental, social and governance factors into account when choosing investments, outperforming the market isn’t one of them. The basic reasoning is that any performance advantage attributable to ESG factors would be quickly arbitraged away. At best, investors attracted to sustainable investing strategies with a view toward achieving positive societal outcomes should expect their investments to achieve total rates of return in line with the market subject to a strategy that also relies on low costs and a combination of indexing along with skilled active management to take advantage of less efficient market segments.

Bloomberg’s Sustainable Finance Article “Stellar Performers”

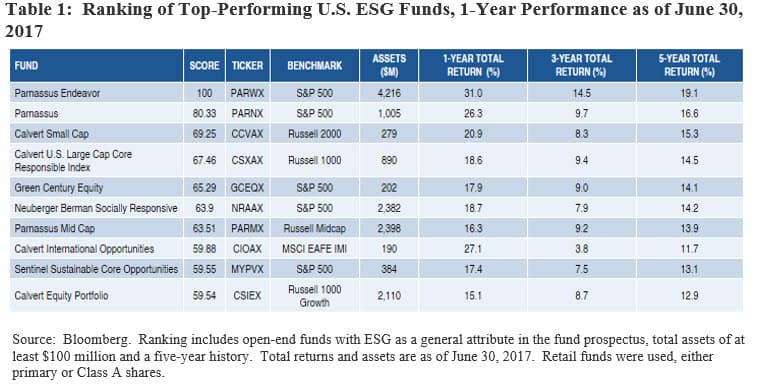

According to Bloomberg’s research, the 10 equity oriented funds with assets of at least $100 million and a five-year history that takes environmental, social and corporate governance factors into account, including eight actively managed funds and two index funds, have proven to be “stellar performers” on the basis of their performance relative to the S&P 500 Index over the 1-year, 3-year and 5-year time intervals. Refer to Table 1 for a complete listing. The top two funds, in particular, beat the S&P 500 Index by wide margins. While the assertion regarding the Parnassus Endeavor Fund and Parnassus Fund is correct, the article suggests that all the funds have been stellar performers. Yet, a more meticulous analysis of these funds along with their investment objectives and policies shows that the results are more nuanced and, in fact, a different outcome emerges regarding the performance of individual funds and the group as a whole.

Evaluating the Performance of the 10 ESG Oriented Funds through a More Appropriate Lens

To further evaluate the performance results of this universe of 10 funds, the following methodology was used:

The evaluation of fund performance was extended to include all share classes rather than focusing the analysis on retail funds only, either primary class or Class A shares. The ten funds and their corresponding share classes include a combined total of 31 funds/share classes. The analysis therefore accounts for the varying expense ratios levied by the funds and reflects the experience of a spectrum of investors served by the funds and ranging from retail to institutional investors. That said, the analysis sidesteps any applicable front-end sales charges where these are applicable. Indeed 5 funds/share classes or 16% of the funds apply a front-end sales charge ranging from a steep 4.5% to 5%. This is highlighted to the extent relevant to understanding the performance results of a given fund.

Fund and share class performance results were evaluated based on each fund’s investment objective and corresponding securities market index, as designated for the fund by the fund management company. That is to say, a benchmark or index corresponding to each fund’s investment objective and strategy is used rather than defaulting to the S&P 500 Index. These indexes are disclosed in each fund’s prospectus and periodic reports. It turns out that the ten funds pursue six different strategies and are evaluated on the basis of six corresponding indexes. In addition to the S&P 500 Index used by 13 funds/share classes for relative performance evaluation purposes, these include the following additional indexes: Russell Mid Cap Index (2 funds/share classes), Russell 1000 Growth Index (4 funds/share classes), Russell 1000 Index (4 funds/share classes), Russell 2000 Index (4 funds/share classes) and the MSCI EAFE SMID Cap Index (4 funds/share classes).

As in the Bloomberg study, performance results were evaluated across the 1, 3 and 5-year intervals through June 30, 2017. In addition, a 10 year time interval has been added.

Observations/Conclusions

The ten funds identified in the Bloomberg article consist of eight actively managed funds as well as two index funds all of which employ sustainable investing strategies that combine exclusionary policies, such as omitting companies with significant involvement in alcohol, tobacco, gambling, military or civilian firearms and nuclear power, as well as more active ESG integration practices. In some cases, sustainable strategies extend to impact investing practices as well as shareholder advocacy/engagement. Generally in line with current practices, the implementation of sustainable investing strategies with regard to methodologies, policies and practices varies from one fund company to the next.

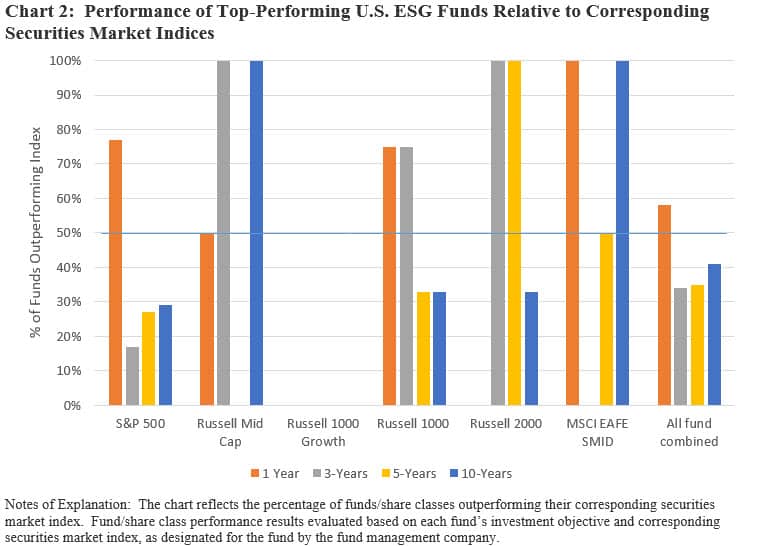

Regardless of strategy, the performance results achieved by the ten funds over the one year period to June 30, 2017 were above average relative to their corresponding indexes and, in some cases, outstanding, as 58% of funds and share classes outperformed their respective benchmarks. In particular, 10 of 13 large cap funds/share classes, or 77% of funds in this group, whose performance is judged against the S&P 500 Index, outperformed the benchmark. Within this group the Parnassus Endeavor Fund and Parnassus Fund generated outstanding 1-year results by exceeding the performance of the S&P 500 Index by between 8.4% and 13.4%, respectively. The near-term results achieved by these two funds and the larger group are likely related to their outsized exposure to the best performing S&P 500 health care and information technology sectors and lower weightings to the worst performing S&P 500 energy sector due to their avoidance of fossil fuel companies. The Parnassus funds with their concentrated portfolios have also distinguished themselves on the basis of longer-term results.

At the same time, the longer term outcomes attained by the universe of the remaining eight funds are less impressive. Over the 3, 5 and 10 year periods to June 30, only 34%, 35% and 41% of the funds, respectively, outperformed their designated securities market indexes. In the case of domestic funds only, the corresponding levels of underperformance are 40%, 32% and 28%, respectively. Refer to Chart 2. While this applies to a small universe of funds, it should be noted that these levels of underperformance are still more favorable by a factor of about 2X when compared to the record achieved by domestic mutual funds more generally. According to research published by S&P Dow Jones Indices in the form of its SPIVA U.S. Scorecard through the end of 2016 for the 3 year, 5 year and ten year intervals, only 7%, 14.2% and 17% of domestic equity funds outperformed their corresponding non-ESG benchmarks[2].

The underperformance of the 8 funds/share classes is, in part, due to the fact that the expense ratios for this universe of funds are high and in some instances, excessively high. The average expense ratio for the retail oriented actively managed subset of funds, a total 18 funds/share classes, is 1.19%. This compares favorably to retail oriented non-sustainable funds with an average expense ratio of 1.25%. That said, only six of the funds/share classes, or 15%, fall within the lowest quartile or the lowest 25% of funds based on management and administrative fees charged (excluding up-front sales charges); and of these, 2 funds are only sold through financial intermediaries while two other fund are subject to $100,000 minimum investments that the management company characterizes as institutional funds. Nine funds/share classes fall within the second and third quartiles while 3 funds fall within the highest quartile with expense ratios in excess of 1.5%. Further, the two index fund offerings charge excessively high fees. These include the Calvert U.S. Large Cap Core Responsible Index that charges fees ranging from 0.54% combined with a 4.5% up front sales charge, and 1.29% for retail oriented purchases while the Green Century Equity Fund charges a fee of 1.25%. While representing an even smaller universe of funds/share classes, institutionally oriented funds are better positioned with 2 out of 4 funds/share classes or 50% falling into the first or lowest quartile relative to an equivalent universe of non-sustainable funds[3].

Admittedly, this analysis is based on a small universe of funds and even as they all take environmental, social and corporate governance factors into account when making investment decisions the individual sustainable policies and practices employed by each of the fund firms varies. Still, the results are more in line with the view that there are many reasons to take environmental, social and governance factors into account when choosing investments, but outperforming the market isn’t one of them. At best, investors attracted to sustainable investing strategies with the intention of achieving a societal benefit should expect their investments, in this case both actively managed funds and passive mutual funds, to achieve total rates of return in line with the market. To the extent that such funds experience intervals of outperformance, contributing factors are just as likely or more likely to be linked to the nature of the asset class as well as fundamental considerations such as market capitalization, growth versus value, geographic exposure, industry, sector and stock selection, in the case of equity funds.

Bottom Line

As is the case with investing more generally, the implementation of a sustainable portfolio strategy predicated on an investor’s goals and objectives involves the deployment of some combination of passively managed as well as actively managed investment funds to take advantage of market segment inefficiencies and the selection of skilled managers that can combine financial and sustainability characteristics with an established and consistent track record offering funds or other investment products, to the extent that these are used, that are effectively priced. In any case, investors have to be clear about their sustainability objectives to ensure that these are properly aligned with their portfolio profiles.

[1] Source: This type of investing could save the world — just don’t expect outperformance, too, Mark Hulbert, published July 29, 2017, in MarketWatch.

[2] Source: S&P Dow Jones Indices. SPIVA U.S. Scorecard, based on performance data through 2016. It should be noted that the relative performance of ESG funds is to June 30, 2017, while SPIVA data runs through 2016.

[3] Expense ratio analysis based on a universe of retail oriented actively managed U.S. equity funds, including large-cap, mid-cap and small-cap funds, for a total of 5,846 funds/share classes, and 1,204 equivalent institutionally oriented funds with minimum initial investments over $100,000. Data source: STEELE Mutual Fund Expert, Morningstar data as of June 30, 2017.