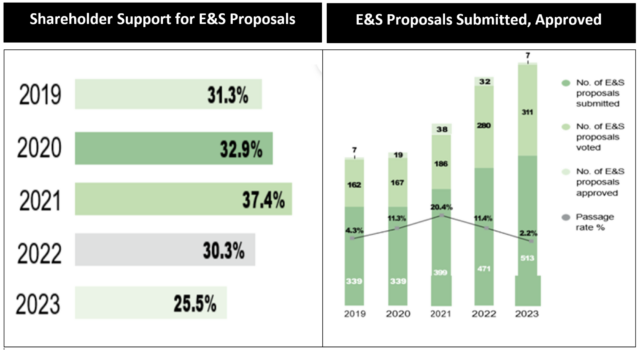

Shareholder support for E&S proposals, submissions and approvals: 2019 – 2023 Notes of explanation: Sources Harvard Law School Forum on Corporate Governance, A Review of the 2023 Proxy Season: An E&S Backlash? posted by Lara Aryani, William Kim, Shearman Sterling LLP, December 21, 2023, with additional sourcing to Broadridge and The Conference Board, Shareholder Voting Trends and Proxy Season Review: Navigating ESG Backlash & Shareholder Proposal Fatigue. The data shown in the chart on the right hand side covers companies constituent of the Russell 3000 index for the full year, except for 2023 in which the period considered was from January 1 through June 30.

Notes of explanation: Sources Harvard Law School Forum on Corporate Governance, A Review of the 2023 Proxy Season: An E&S Backlash? posted by Lara Aryani, William Kim, Shearman Sterling LLP, December 21, 2023, with additional sourcing to Broadridge and The Conference Board, Shareholder Voting Trends and Proxy Season Review: Navigating ESG Backlash & Shareholder Proposal Fatigue. The data shown in the chart on the right hand side covers companies constituent of the Russell 3000 index for the full year, except for 2023 in which the period considered was from January 1 through June 30.

Notes of explanation: Sources Harvard Law School Forum on Corporate Governance, A Review of the 2023 Proxy Season: An E&S Backlash? posted by Lara Aryani, William Kim, Shearman Sterling LLP, December 21, 2023, with additional sourcing to Broadridge and The Conference Board, Shareholder Voting Trends and Proxy Season Review: Navigating ESG Backlash & Shareholder Proposal Fatigue. The data shown in the chart on the right hand side covers companies constituent of the Russell 3000 index for the full year, except for 2023 in which the period considered was from January 1 through June 30.