The Bottom Line: Focused sustainable fund assets recorded their best monthly gain to-date, fund launches remained moribund and the relative performance of ESG indices improved.

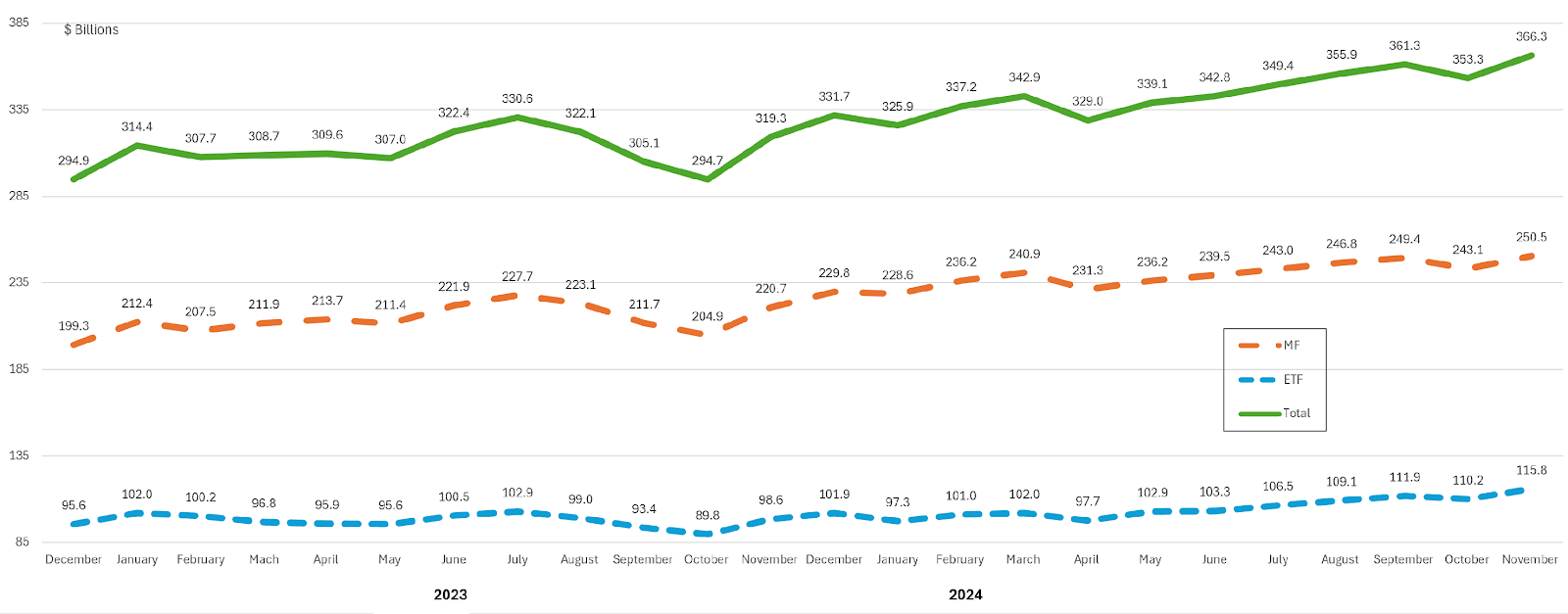

Long-Term Net Assets: Sustainable Mutual Funds and ETFs |

Focused sustainable long-term fund assets under management attributable to mutual funds and ETFs (excluding money market funds), 1,392 funds/share classes in total (1,159 mutual funds/share classes and 233 ETFs), based on Morningstar classifications, closed the month of November with $366.3 billion in net assets. This represents a net increase of $13.1 billion, attributable to capital appreciation as well as net inflows, for a gain of 3.7%. At $13.1 billion, this is also the best gain so far this year as it surpassed the $11.3 billion increase recorded in February 2024. The net assets of both sustainable mutual funds as well as ETFs experienced increases, reaching $250.5 billion and $115.8 billion, respectively. Based on a simple calculation that reflects the average November total returns registered by long-term funds, combining mutual funds and ETFs, of almost 3.0%, an average return of 2.92% posted by long-term mutual funds and 3.16% by ETFs, it is estimated that sustainable funds in the aggregate experienced cash inflows during November in the amount of $730.1 million. Mutual funds added about $7.4 billion in November, including $300 million in net cash inflows. ETFs added about $5.7 billion, including positive flows in the amount of $2.2 billion. Since the start of the year, focused sustainable mutual funds and ETFs have added a combined net of $34.6 billion in assets, for an increase of 10.0%. Mutual funds accounted for about 60% of the net gain. |

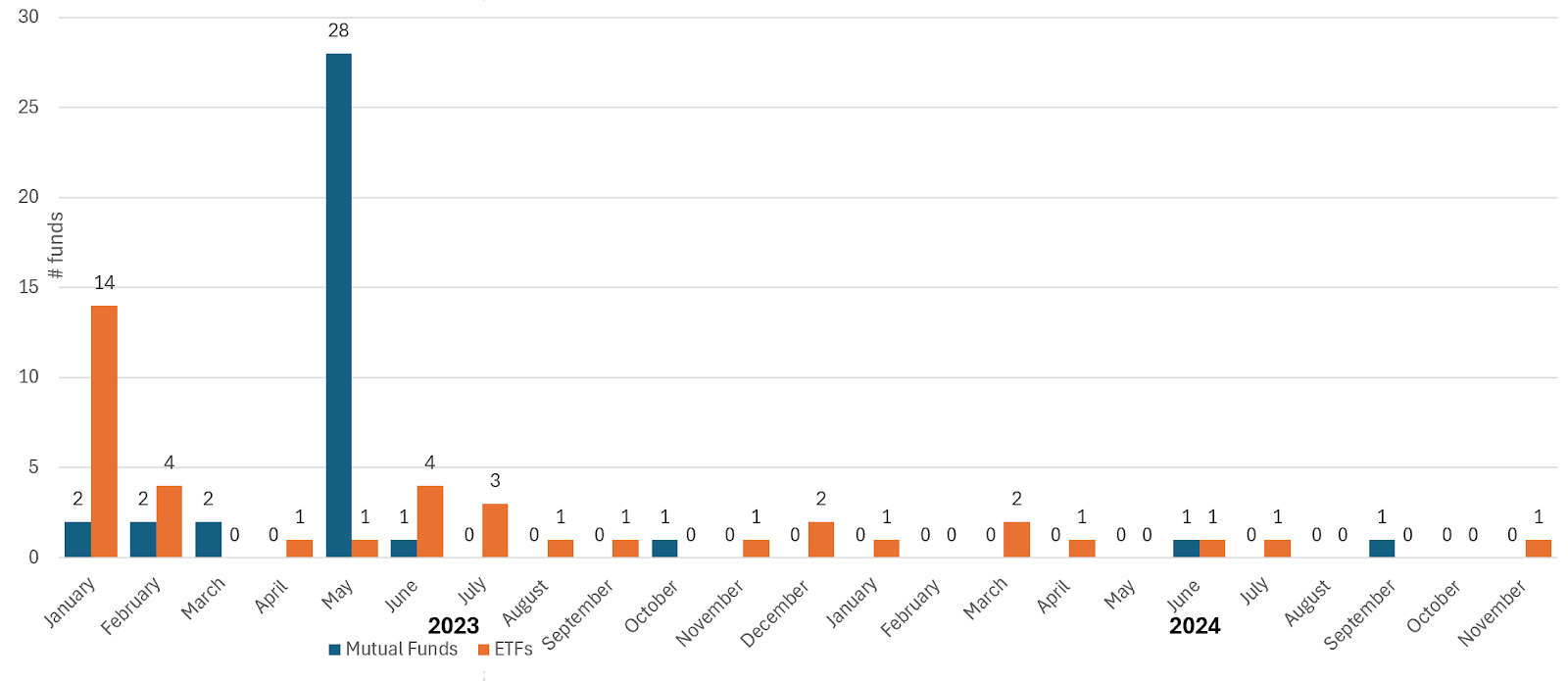

New Sustainable Fund Launches |

The drought affecting new listings of focused sustainable funds, which started after May of last year, continued into November 2024. There were no new mutual fund listings in November, however, one new sustainable ETF was launched in the latest month. The new ETF launch was offset by two ETFs that were delisted as well as three mutual fund closings in November. In the latest full month, focused sustainable long-term funds added $13.1 billion in net assets to reach $366.3 billion, for a 3.7% gain, attributable to capital appreciation and positive cash flows. This was the segment’s best overall monthly gain so far this year, exceeding the next best uptick that was observed in March when combined long-term assets reached 342.9 billion. Long-term funds gained an average of almost 3.0% in November and 18.0% over the trailing twelve months. The newest ETF is a $17.3 million index fund managed by Empowered Funds dba ETF Architect dba EA Advisors (owned by Alpha Architect, LLC), a Pennsylvania-based manager with $8.5 billion in assets under management, and sub-advised by Stance Capital. The Stance Sustainable Beta ETF (STSB) seeks to replicate the performance of the Change Finance Diversified Impact U.S. Large Cap Fossil Fuel Free Index. The index is constructed around 100 large-, mid-capitalization equity securities of U.S.-listed companies, selected from a universe of 1,000 firms that excludes companies involved in the fossil fuel industry, fossil-fired utilities and companies which fail to meet a diverse set of environmental, social, and governance criteria established by Change Finance using, but not relying exclusively, on ESG data provided by ISS ESG data. In addition, the sub-adviser may engage in shareholder activism with respect to the fund’s holdings by sending letters, engaging in dialog with company management and possibly submitting shareholder proposals on a variety of ESG-related issues, including those related to the ESG factors. Since the start of the year, there have been only nine new mutual fund ETFs listings, versus a combined total of 66 over the same time interval (based on slightly revised data). |

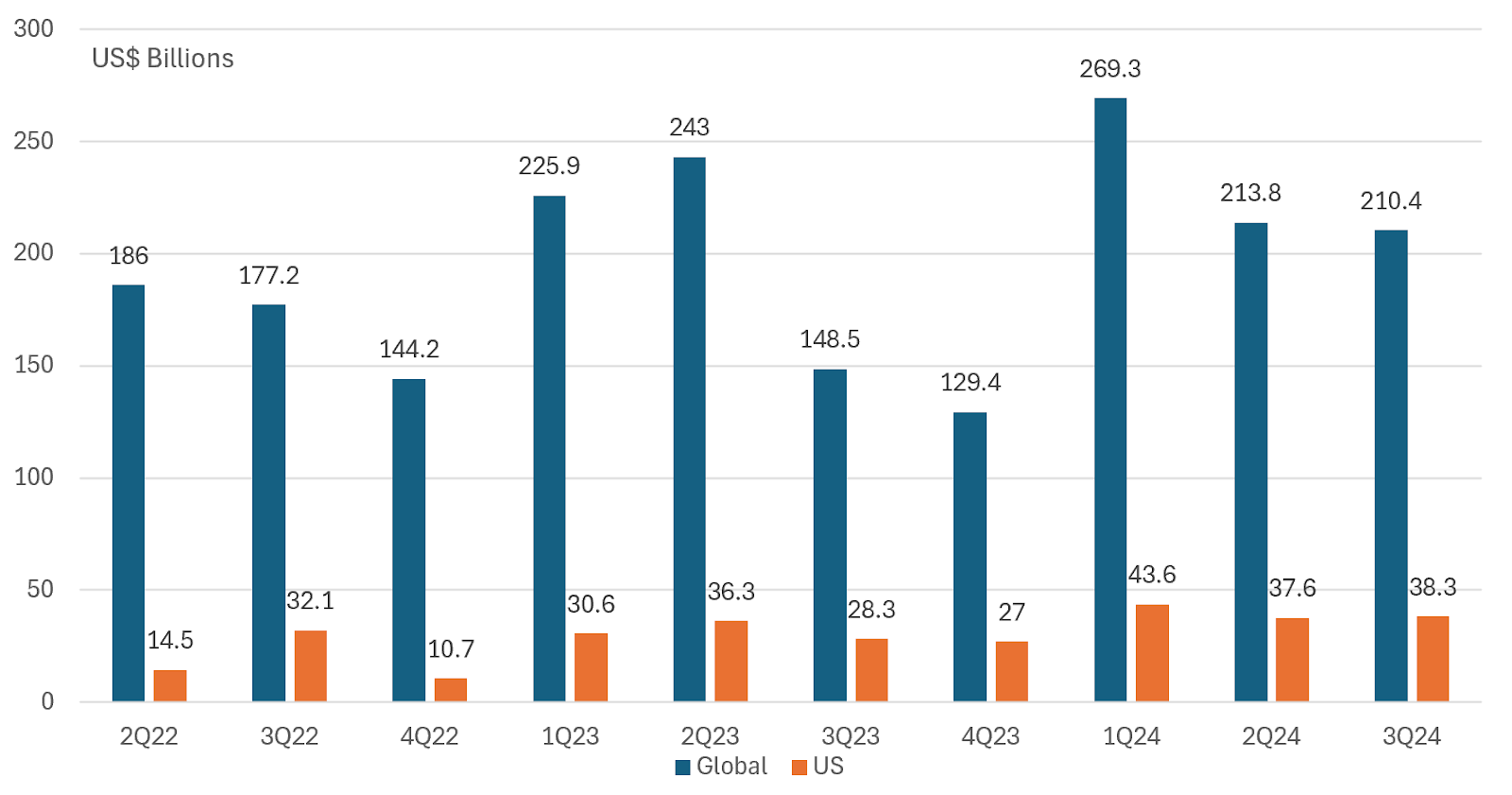

Green, Social and Sustainability Bonds Issuance (to Q3 2024) |

While consistent and reliable Q4 and annual 2024 issuance data will not be available for several weeks following year-end, two benchmarks in the form of forecasts are worth keeping in mind as the data rolls in. The first is S&P Global’s projection, made early in the year, that annual issuance of green, social, sustainability, and sustainability-linked bonds could reach $1.05 trillion in 2024 and account for 14% of global issuance. The second is a slightly more modest $950 billion forecast offered by Moody’s Investors. Even at the high end of the range, issuance would still fall below the high level of almost $1.1 trillion recorded in 2021. SIFMA Q3 2024: Issuance data through the end of October is not yet available, but last month SIFMA released third quarter data showing that global green, social and sustainable bond issuance in the third quarter of 2024 reached $210.4 billion. Based on slightly adjusted issuance numbers for the second quarter, this represents a quarter-over-quarter decline of $3.4 billion, or a 1.6% drop. Green bonds accounted for 57.9% of global issuance while sustainability bonds and social bonds represented 25.4% and 16.7%, respectively, of total issuance. Global issuance year-to-date reached $693.5 billion, running ahead of the comparable period last year when volume reached $617.4 billion or over the comparable period in 2023. This represents a $76.1 billion pick up in sustainable bond issuance, or an increase of 12.3%. Against a backdrop of another strong quarter when fixed income issuance in the US reached $2.9 trillion, or a quarter over quarter increase of 16.1%, US sustainable bond issuance in the third quarter came in at $38.3 billion, recording a modest $0.7 billion increase, or 1.9%. Year-to-date, US sustainable bond issuance reached $119.5 billion, for a year-over-year increase of $24.3 billion or 24.3%. It should be noted that SIFMA data tends to understate global sustainable bond issuance as it captures a narrower slice of the market that also includes sustainability linked bonds and notes, for example. More generally, sustainable bond data provided by different data sources can vary by significant margins. |

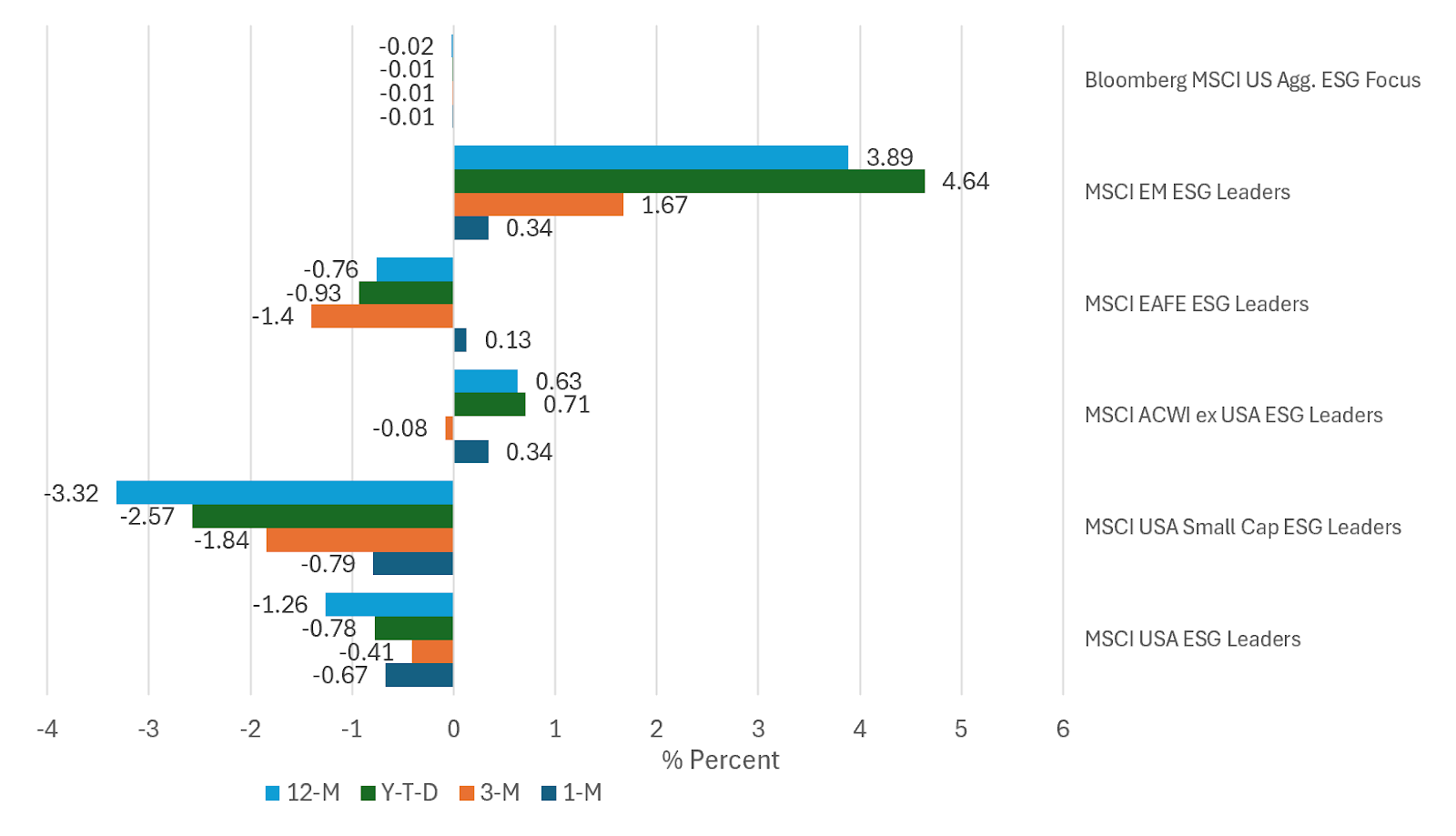

Short-Term Relative Performance: Selected ESG Indices vs. Conventional Indices |

November’s U.S. presidential election, which had been too-close to-call, resulted in a clear victory for Donald Trump and Republican majorities in both the Senate and the House of Representatives. The election outcomes ignited a broad-based post-election stock market rally that produced the best monthly return so far this year for stocks. The S&P 500 added 5.9% on a total return basis. Market sentiment remains very positive, but the index is now trading at a stretched PE of 25.79 X estimated 2024 earnings. The Dow Jones Industrial Average (DJIA), which posted seven new closing highs in November, also ended the month with a closing high of 44,910.65. The DJIA gained 7.7% while the Nasdaq 100 posted an increase of 5.3%. Small and mid-cap growth indices were some of the best performers in November, with the Russell Mid Cap Growth Index and Russell 2000 Index posting very strong gains of 13.3% and 12.3%, respectively. The Russell 2000 registered its best monthly gain since December 2023, adding almost 11% and recording a gain of 21.6% over the trailing 12-months versus an increase of 29.1% for the S&P 500. International equity indices moved in the opposite direction. The MSCI ACWI ex USA gave up 0.91% in November but maintained a positive result since the start of the year with a gain of 8.34%. This reflected the drag of emerging markets that posted a decline of 3.59% according to the MSCI Emerging Markets Index—driven by declines recorded in Brazil (-7.1%), Korea (-5.7%) and China (-4.4%) At the same time, against a backdrop of flagging growth in Europe, the developed markets MSCI EAFE Index managed to limit its decline to 0.57% and a year-to-date drop of 6.24% even as France dropped 4.2%. Inflation remains above the Federal Reserve’s 2% target, and recent data shows that it is still a thorn. Nevertheless, the Federal Reserve, based on CME probability figures, is expected to cut interest rates by 25 basis points at the scheduled December 17-18 meeting, despite a slight increase in inflation in November. Long-term interest rates in November stabilized and shifted from a high yield of 4.44% attributable to 10-year Treasuries to 4.18% at month-end. At the same time, the Bloomberg US Aggregate Bond Index gained 1.06% and 2.93% since the start of the year. Long-term credit instruments, such as the Bloomberg US Long Credit Total Return Index gained 2.21% and 2.28% year-to-date. Long-term focused sustainable funds (excluding money market funds recorded an average gain of almost 3.0% and, for the trailing 12-months, grew by an average of 18%. A selection of five US and international equity ESG Leaders indices and one fixed income benchmark, for a total of six benchmarks constructed by MSCI around ESG screening and exclusionary criteria, improved their relative monthly performance results in November versus October. All three international equity-oriented ESG Leaders indices outperformed their conventional counterparts in November, recording excess returns ranging from 13 basis points (bps) recorded by the MSCI EAFE ESG Leaders Index to 34 bps achieved by the MSCI ACWI ex USA ESG Leaders Index as well as the MSCI Emerging Markets ESG Leaders Index. At the same time, the two US-oriented benchmarks, the MSCI USA ESG Leaders Index and the MSCI USA Small Cap ESG Leaders Index underperformed by 67 bps and 79 bps respectively while the fixed income-oriented index, the Bloomberg MSCI US Aggregate ESG Focus Index, lagged by a very narrow 1 bps. Beyond the one-month results and continuing to 12-months, relative performance results over the 3-, 11- and 12-month intervals registered by the ESG-oriented benchmarks lagged, with the exception of the MSCI Emerging Markets Leaders Index that outperformed during each of the three intervals. Over the intermediate and long-term time frames, relative performance results through November remain lackluster. Equity and fixed income ESG indices lagged their conventional benchmarks over the three-year period. Over the previous five years, only two indices outperformed. At the same time, three of the five (the track record of fixed income securities doesn’t extend to 10 years) ESG indices outperformed their conventional benchmarks. These include the three international yardsticks. That said, the ten 10-year track record attributed to ESG indices is questionable in the light of significant operational and definitional changes over that time interval. 3-year and 5-year proxies may be better indicators. |

Sources: Morningstar Direct, MSCI, SIFMA/Dealogic and Sustainable Research and Analysis LLC