![Monitor-1-istockphoto-1437090010-612x612-3[1]](https://sustainableinvest.com/wp-content/uploads/elementor/thumbs/Monitor-1-istockphoto-1437090010-612x612-31-2-rd4j6zu5zslj4d8s6wocofhr6mjtkms5pf87wwo4h8.jpg "Monitor-1-istockphoto-1437090010-612×612-3[1]")

The Bottom Line: Sustainable funds gave up assets again in April while green bonds flourished. Relative performance results were mixed, and fund launches remained muted.

|

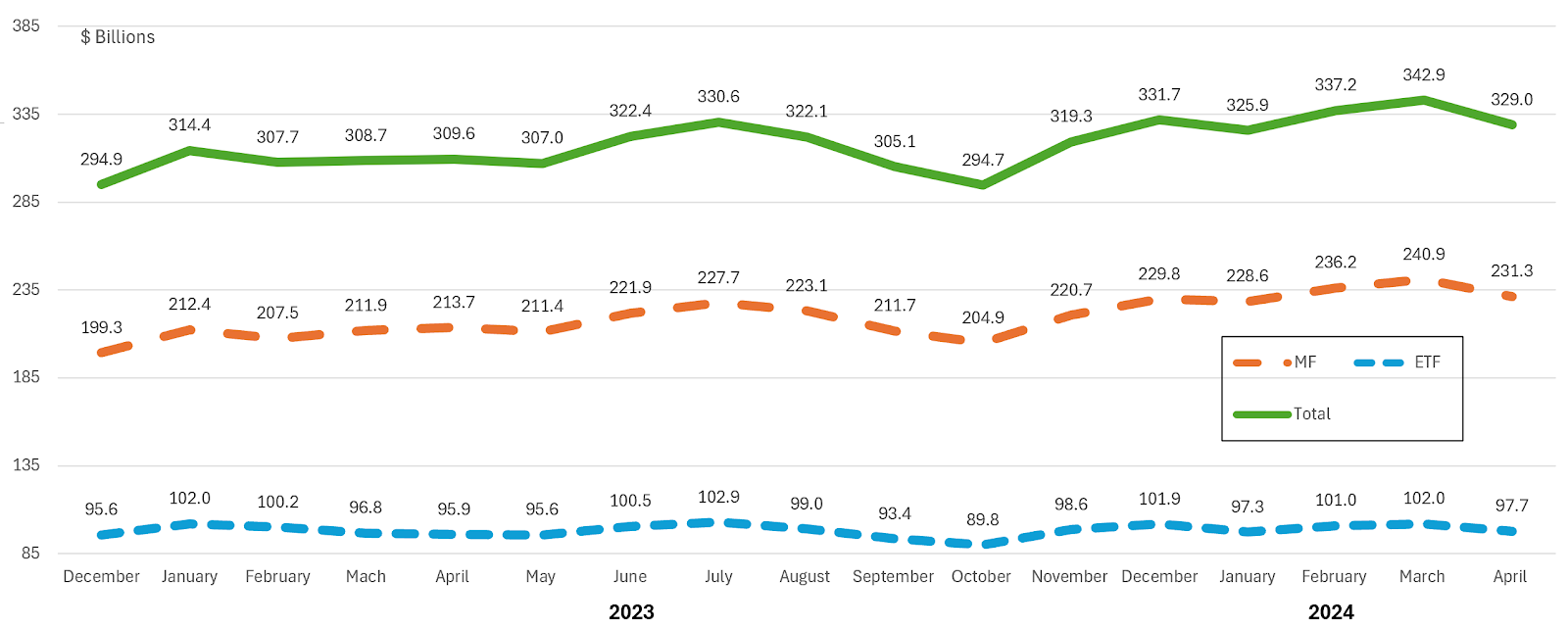

Long-Term Net Assets: Sustainable Mutual Funds and ETFs |

|

Sustainable long-term fund assets under management attributable to mutual funds and ETFs, 1,506 funds/share classes (focused funds) in total, based on Morningstar classifications, closed the month of April at $329 billion in net assets. This represents a month-over-month decrease of $13.9 billion, or a 4.1% decline and a year-to-date drop of $2.7 billion. Based on a simple calculation that reflects the average -3.2% total return recorded by long-term funds in April, it is estimated that sustainable funds experienced net cash outflows in the amount of $2.9 billion. Mutual funds, which are still ahead relative to December 31st by a narrow $1.5 billion, sustained an estimated $2.0 billion in outflows. At the same time, the assets of the ETF segment dropped below their year-end 2023 high level and recorded estimated outflows of $0.9 billion in April. |

|

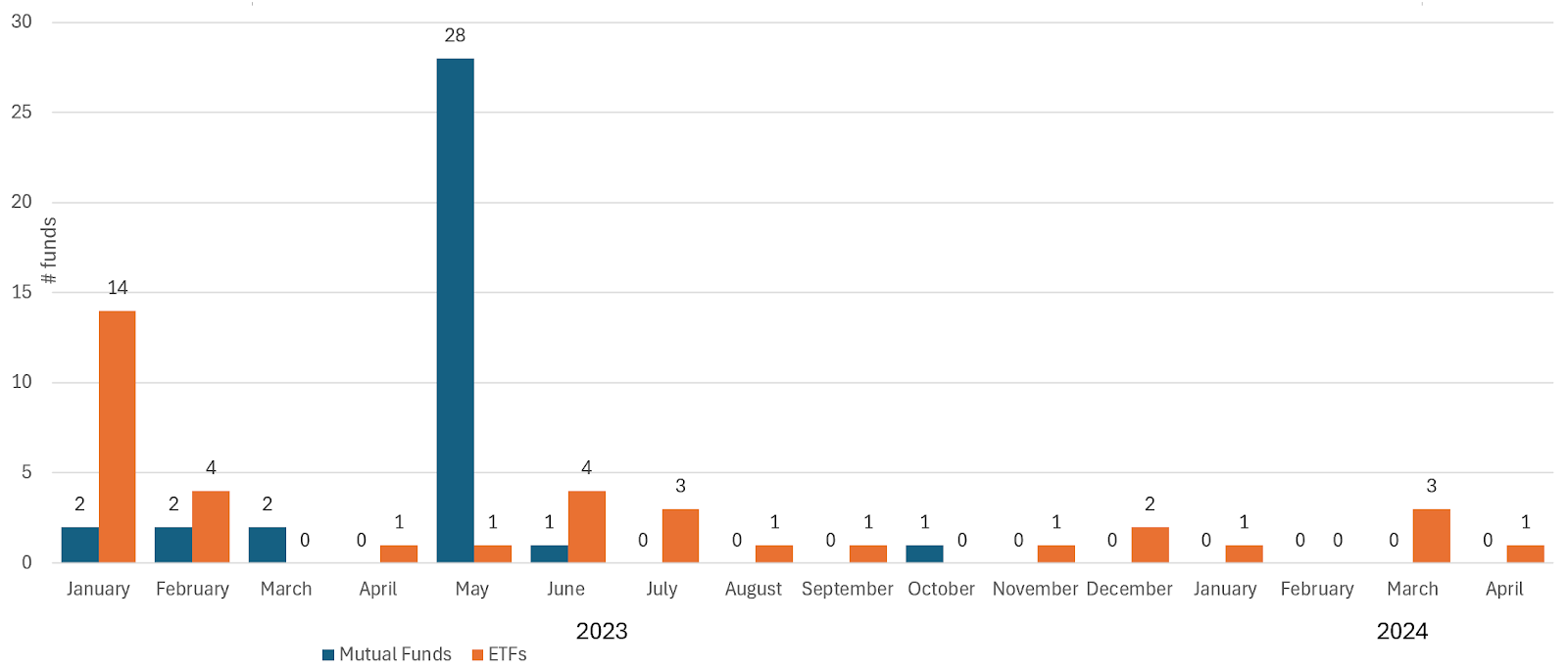

New Sustainable Fund Launches |

|

The cooling off in sustainable fund introductions continued into April when only one sustainable ETF was launched. The new fund, Carbon Collective Short Duration Green Bond Fund, managed by Tidal Investments LLC and sub-advised by Carbon Collective Investing, LLC as well as Artesian Capital Management (Delaware) LP, is the first green bond fund to have been introduced since the launch of the rebranded Franklin Liberty Federal Tax-Free Bond ETF, renamed the Franklin Municipal Green Bond ETF, as of May 3, 2022. During the year-to-date interval, there have been no new mutual fund listings. Averaging just 1 new fund introduction per month in 2024, this compares to an average of 11 monthly listings in 2023 up to May of the same year. Thereafter, the average for the next seven months dropped to two new fund listings per month. This development may be linked to the anti-ESG movement in the US that had gained momentum in the second quarter of 2023 and fund companies may have opted to lower their profile by curtailing focused fund offerings. At the same time, commitments to ESG integration does not appear to have subsided, based on reporting by the largest fund companies. |

|

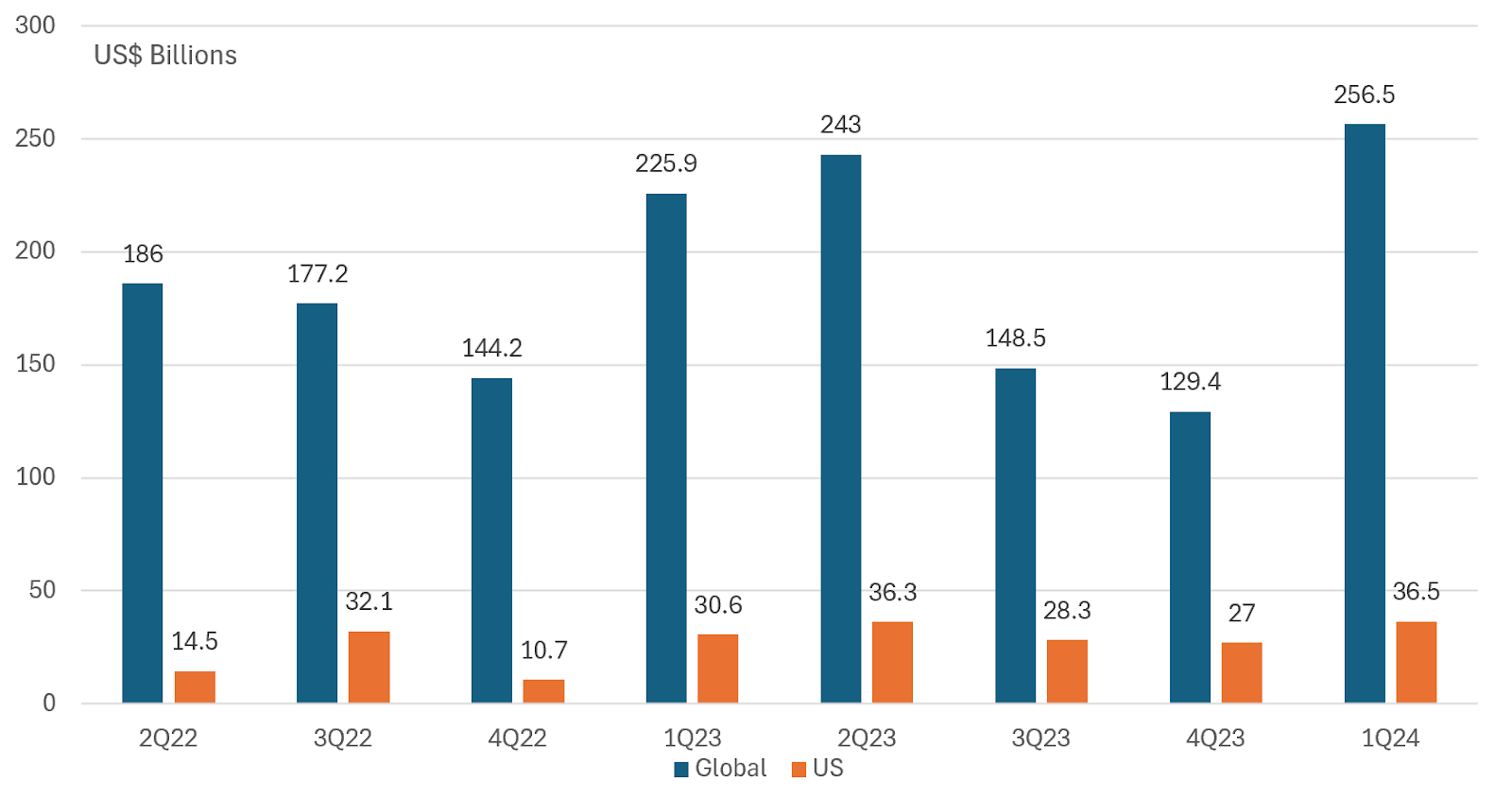

Green, Social and Sustainability Bonds Issuance |

|

According to the latest data provided by SIFMA, global green, social and sustainable bond issuance in the first quarter of 2024 rose to $256.5 billion, for a Q/Q $127.9 billion increase or nearly doubling of the issuance level recorded during the previous quarter. January was the strongest month, during which $123.2 billion in green, social and sustainability bonds were issued—led by green bonds over the quarter (but not in the US where sustainability bonds dominated). Issuance volumes moderated in February and March. U.S. issuance gained too, reaching $36.5 million for a Q/Q gain of 35% and exceeding the previous 2Q 2023 quarterly high mark since early 2022. This came on the heels of strong Q1 aggregate issuance levels for bonds in the US that saw an increase of $2.5 trillion for a 26% gain. Other reports covering sustainable debt volumes in the first quarter 2024 quote even higher volume numbers. Moody’s, for example, in a report issued on May 1 reported that issuance rose by 36% in the first quarter to $281 billion. Total issuance was up from $207 billion in the fourth quarter, and more or less in line with the same quarter a year ago. The report also noted that the green-bond segment led the way with $169 billion worth of new issue activity, followed by $55 billion of sustainability bonds, $48 billion in social bonds, and $10 billion of sustainability-linked bonds. One of the reasons for the variation relative to SIFMA data is attributable to the inclusion of sustainability-linked bonds, a segment of the sustainable debt instruments market that has been subject to regular criticism from analysts and asset managers who note that the bond targets are weak, they are more likely to be missed and are hard to monitor. |

|

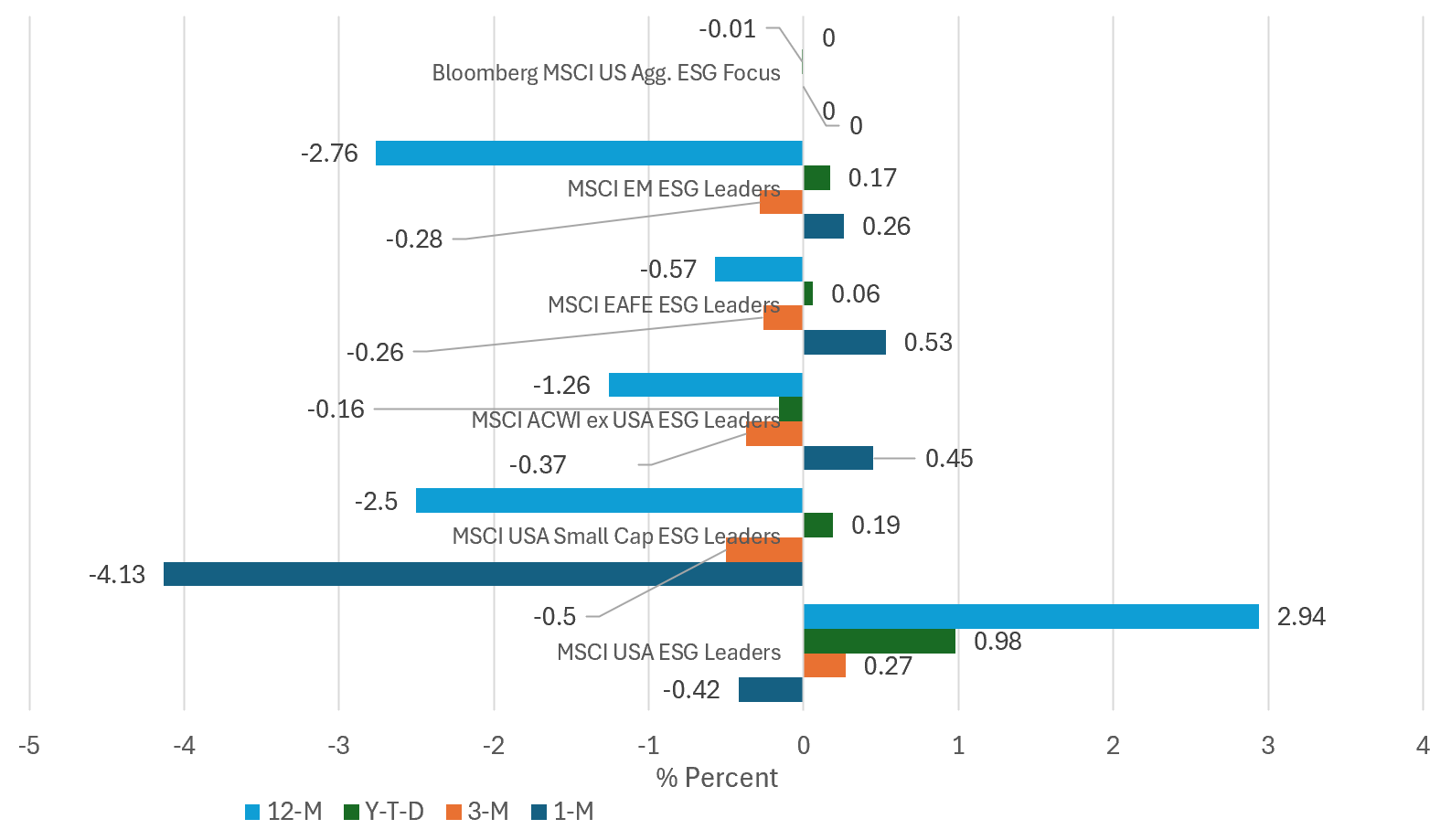

Short-Term Relative Performance: Selected ESG Indices vs. Conventional Indices |

|

Investor optimism during the first quarter of the year shifted to lower gear in April as investors came to realize that interest rates are not likely to move lower any time soon and Middle East tensions escalated. At the same time, corporate earnings came in above the 1% estimated gain and provided some ballast to the equity market. All three major indices declined in April, with large cap growth stocks outperforming value stocks but the reverse was true for small cap stocks. The S&P 500 Index recorded a 4.08% decline while the Russell 2000 Index, consisting of small companies, dropped even lower, giving up 7.04%. After finally recording a monthly gain of 0.9% in March, bonds sold off as 10-year Treasury’s posted the highest yield so far this year, ending the month at 4.69% versus 4.20% as of March 28, 2024. US investment-grade intermediate bonds, as measured by the Bloomberg US Aggregate Bond Index, dropped 2.53% and registered a wider decline of 3.28% year-to-date. Outside the U.S., the MSCI ACWI ex U.S. registered a decline of 1.8%, benefiting from the stronger performance in emerging markets that recorded an increase of 0.45%. Against this backdrop, April’s performance of a selection of five US and international equity ESG Leaders indices and one fixed income benchmark, relative to their conventional counterpart indices as calculated by MSCI, reflected mixed results. Three benchmarks tracking international markets, the MSCI ACWI ex USA ESG Leaders Index, the MSCI EAFE ESG Leaders Index and the MSCI Emerging Markets ESG Leaders Index beat their conventional counterparts in April by a range between 26 basis points (bps) and 53 bps. At the same time, the performance of sustainable bonds was in line with conventional bonds while two U.S focused ESG indices, one tracking large and mid-cap companies and the other small cap companies, trailed their conventional counterparts. While relative results across the six indices improved on a year-to-date basis, this is not the case across the trailing twelve months during which interval only one of six benchmarks outperformed. Over the intermediate three-to-five-year time intervals, relative performance results were mixed while over the long-term, covering just five of the six ESG Leaders indices, four of the five indices outperformed. |

Sources: Morningstar Direct, Bloomberg, MSCI, SIFMA/Dealogic and Sustainable Research and Analysis LLC