The Bottom Line: Sustainable fund assets declined due to market drops, offset by modest positive flows, while fund launches remain moribund and ESG indices underperformed.

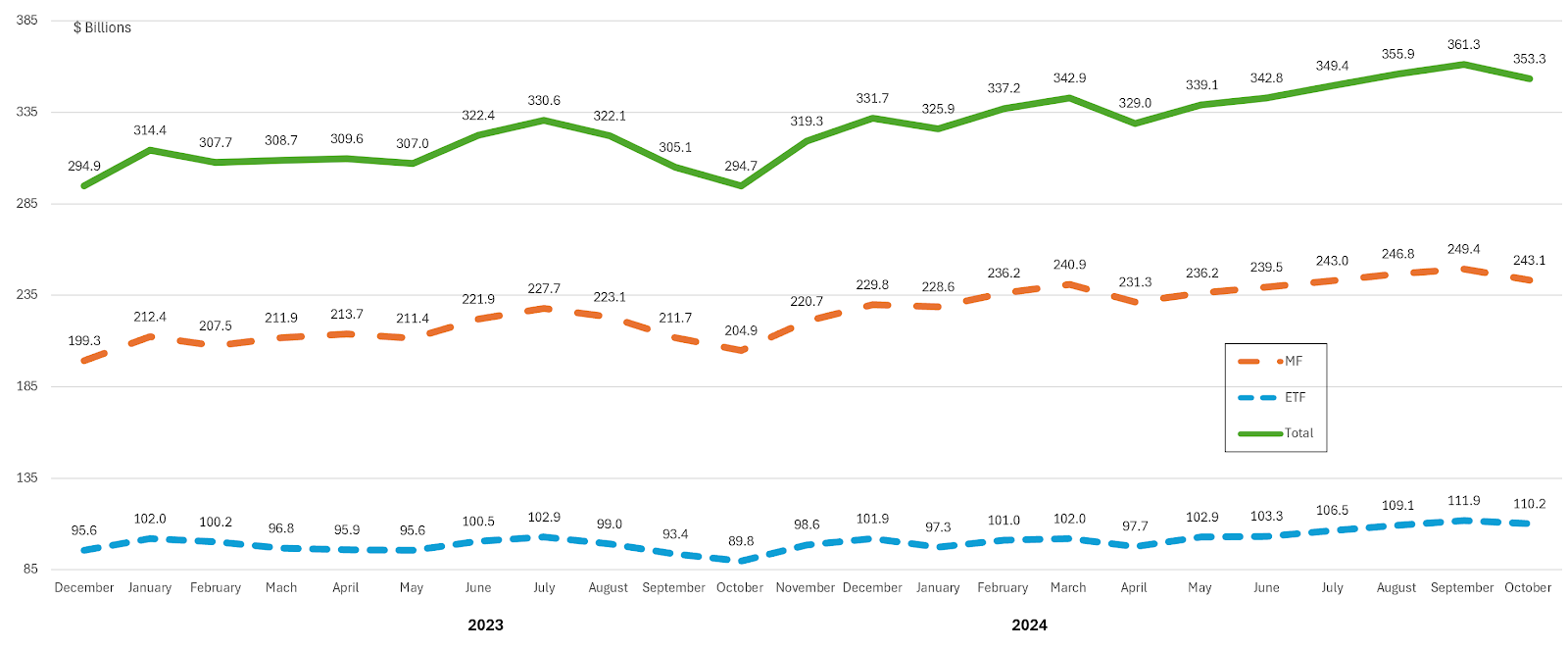

Long-Term Net Assets: Sustainable Mutual Funds and ETFs |

Focused sustainable long-term fund assets under management attributable to mutual funds and ETFs (excluding money market funds), 1,404 funds/share classes in total (1,169 mutual funds/share classes and 235 ETFs), based on Morningstar classifications, closed the month of October with $353.3 billion in net assets. This represents a net decline in assets of $8.02 billion, or a drop of 2.2%, and the first monthly decline since April of this year. The declines are attributable to a combination of capital depreciation due to drops in both the stock and bond markets as well as positive cash flows. The net assets of both sustainable mutual funds as well as ETFs experienced decreases, reaching $243.1 billion and $110.2 billion, respectively. Based on a simple calculation that reflects the average October total returns recorded by long-term funds, combining mutual funds and ETFs, of -2.64%, long-term mutual funds at -2.55% and -3.11% by ETFs, it is estimated that sustainable funds in the aggregate experienced cash inflows during October in the range between $1.5 billion and $1.9 billion. Mutual funds experienced cash inflows of about $100 million while ETFs registered inflows estimated at around $1.8 billion. Since the start of the year, focused sustainable mutual funds and ETFs have added a combined net of $21.6 billion in net assets, for an increase of 6.5%. Mutual funds accounted for about 62% of the net gain. |

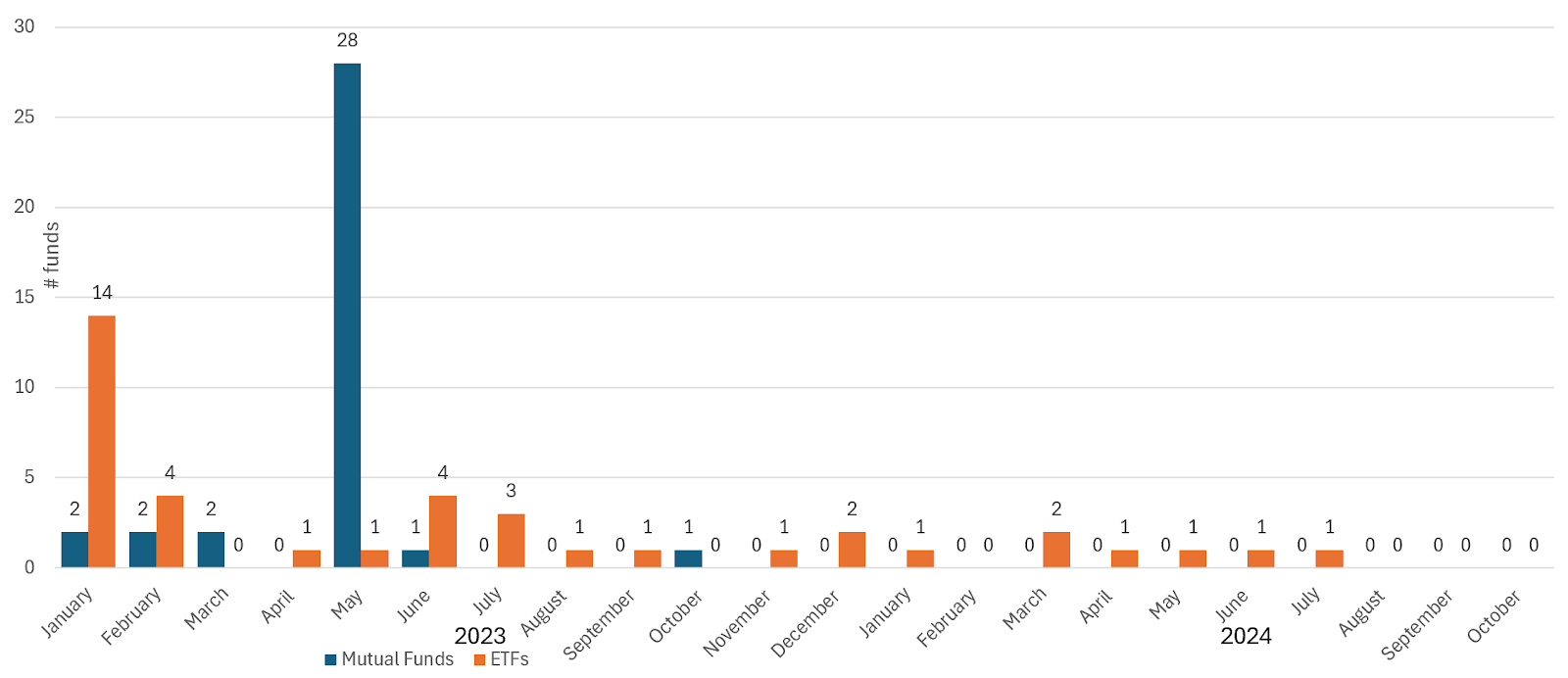

New Sustainable Fund Launches |

The drought affecting new listings of focused sustainable funds, which started after May of last year, continued into October 2024. There were no new mutual fund or ETF listings during the month. Year-to-date, there were seven ETF listings, as compared to 65 listings during the same period in 2023, comprised of 36 mutual funds/share classes and 29 ETFs. During the month, there were two sustainable ETF liquidations, including the Janus Anderson International Equity ETF and the Nuveen Global Net Zero Transition ETF, with about $7.4 million and $6.6 million in net assets, respectively. There were also four mutual fund liquidations, including the Allspring Municipal Sustainable Fund ($24.8 million), BlackRock Life Path ESG Index Fund 2025 ($3.7 million), Nine One Global Environmental Fund ($25.6 million) and Transamerica Sustainable Bond ($23 million). Fund reorganizations are excluded. The scarcity in sustainable fund launches, starting after May of last year, may be attributable to the fact that anti-ESG movement in the US had gained momentum in the second quarter of 2023 and fund companies may have opted to lower their profile by curtailing focused fund offerings while at the same time continuing to support sustainable investing practices. Sustainability also remains important to corporate executives as well as asset owners. According to the previous month’s Voice of the Asset Owner Survey 2024 report by published by Morningstar based on survey findings, 67% of asset owners globally say that “ESG has become more material in the last five years.” The US presidential election results may stimulate demand for focused sustainable mutual funds and ETFs. Retail and institutional investors might feel galvanized by the election of Donald Trump to express their concern about environmental and social issues, such as climate change, racial equity, and corporate responsibility. In its own way, fund family exits from the focused sustainable funds sphere may also be reflecting the pause that has affected new sustainable fund listings. Since the start of the year and continuing to October 31, 2024, 18 fund firms, or 11% of firms offering focused sustainable funds as of the start of 2024, terminated their sustainable fund offerings. These exclude fund firms that were acquired, merged or consolidated with other firms. |

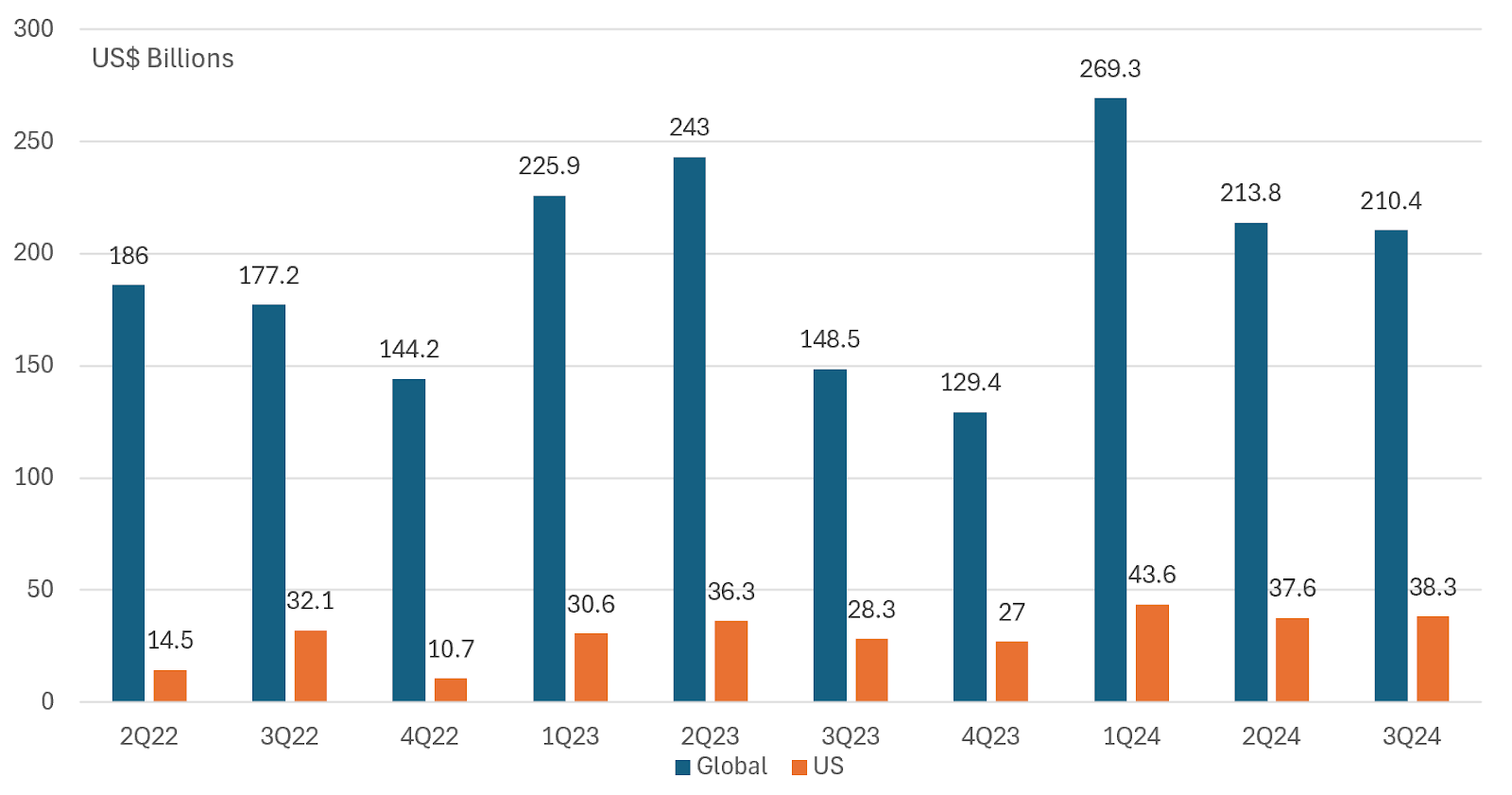

Green, Social and Sustainability Bonds Issuance (to Q3 2024) |

Issuance data through the end of October is not yet available, but last month SIFMA released third quarter data showing that global green, social and sustainable bond issuance in the third quarter of 2024 reached $210.4 billion. Based on slightly adjusted issuance numbers for the second quarter, this represents a quarter-over-quarter decline of $3.4 billion, or a 1.6% drop. Green bonds accounted for 57.9% of global issuance while sustainability bonds and social bonds represented 25.4% and 16.7%, respectively, of total issuance. Global issuance year-to-date reached $693.5 billion, running ahead of the comparable period last year when volume reached $617.4 billion or over the comparable period in 2023. This represents a $76.1 billion pick up in sustainable bond issuance, or an increase of 12.3%. Against a backdrop of another strong quarter when fixed income issuance in the US reached $2.9 trillion, or a quarter over quarter increase of 16.1%, US sustainable bond issuance in the third quarter came in at $38.3 billion, recording a modest $0.7 billion increase, or 1.9%. Year-to-date, US sustainable bond issuance reached $119.5 billion, for a year-over-year increase of $24.3 billion or 24.3%. It should be noted that SIFMA data tends to understate global sustainable bond issuance as it captures a narrower slice of the market that also includes sustainability linked bonds and notes, for example. More generally, sustainable bond data provided by different data sources can vary by significant margins. |

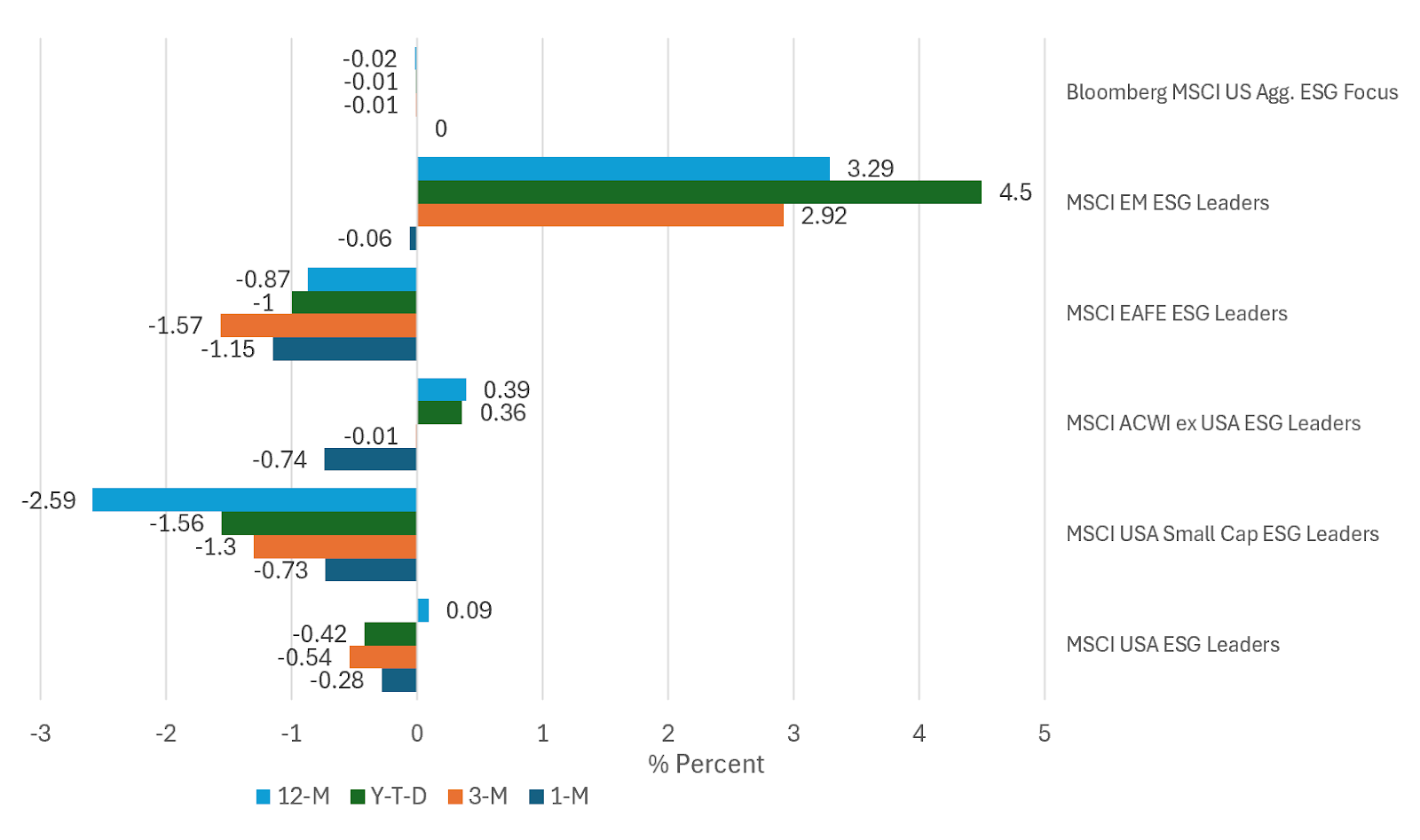

Short-Term Relative Performance: Selected ESG Indices vs. Conventional Indices |

For the month, the benchmark S&P 500 fell over 0.91% on a total return basis, reversing course following five consecutive monthly gains. For the year-to-date interval and trailing twelve months, the index recorded strong gains of 20.97% and 38.02%, respectively. The Dow Jones Industrial Average gave up 1.26% in October and it also fell behind the S&P 500 for the year-to-date period as well as trailing 12-months with lower gains of 12.5% and 28.85%, respectively. Growth stocks outperformed their value counterparts but fell 1.8% on the month. Financials (2.7%), communications services (1.9%) and energy 0.8%) produced the only gains while health care (-4.6%), materials (-3.5%) and real estate (-3.3%) recorded the largest sector drops. Small caps retraced by 2.7%, as slowing economic momentum continued to weigh on the segment. Foreign markets, as measured by the MSCI ACWI ex US Index, declined 4.91% while emerging markets, as calculated by the MSCI Emerging Markets Index, gave up 4.45%. A run of five consecutive monthly gains was also halted for bonds, as the Bloomberg US Aggregate Bond Index recorded a significant drop of 2.48% in October. Focused sustainable mutual funds and ETFs registered an average decline of 2.63% while long-term funds only (excluding money market funds), were down 2.64%. Year-to-date and over the trailing twelve months, average returns were 8.97% and 23.45%, respectively. Long-term mutual funds outperformed ETFs only, posting average returns of -2.55% and -3.11%, respectively, due in large part to their varying exposures/profiles. Sustainable US equity funds gave up an average of 1.63% while the results achieved by international equity funds were even worse, down an average of 4.23%. Bond funds suffered a significant decline that was just two basis points behind US equity funds, recording an average decline of 1.61%. Year-to-date the three categories recorded gains of 15.28%, 8.85% and 3.58%, respectively. Over the trailing twelve months, average results were 33.68%, 25.28% and 11.0%, respectively. A selection of five US and international equity ESG Leaders indices and one fixed income benchmark, for a total of six benchmarks constructed by MSCI around ESG screening and exclusionary criteria, turned in the worst relative monthly performance results so far this year. All five equity-oriented ESG Leaders indices trailed their conventional counterparts in October, lagging by range from 6 bps recorded by the MSCI Emerging Markets ESG Leaders Index to a high of 115 bps registered by the MSCI EAFE ESG Leaders Index. A contributing factor was the outperformance of the energy sector and the underperformance of the technology sectors. At the same time, the Bloomberg MSCI US Aggregate ESG Focus Index delivered a return equivalent to its conventional counterpart. Beyond the one-month results and continuing to 12-months, relative performance results improved, with up to 50% of the equity indices outperforming while the ESG fixed income benchmark lagged by the smallest of margins over the 3-month, year-to-date and 12-month intervals. Over the intermediate and long-term time frames, relative performance results through October are mixed. Equity and fixed income ESG indices lagged their conventional benchmarks over the three-year period. Over the previous five years, only two indices outperformed. At the same time, four of the five (the track record of fixed income securities doesn’t extend to 10-years) ESG indices outperformed their conventional benchmarks while US large and mid-cap stocks underperformed. That said, the ten 10-year track record attributed to ESG indices is questionable in the light of significant operational and definitional changes that time interval. 3-year and -year proxies may be better indicators. |

Sources: Morningstar Direct, MSCI, SIFMA/Dealogic and Sustainable Research and Analysis LLC