Introduction

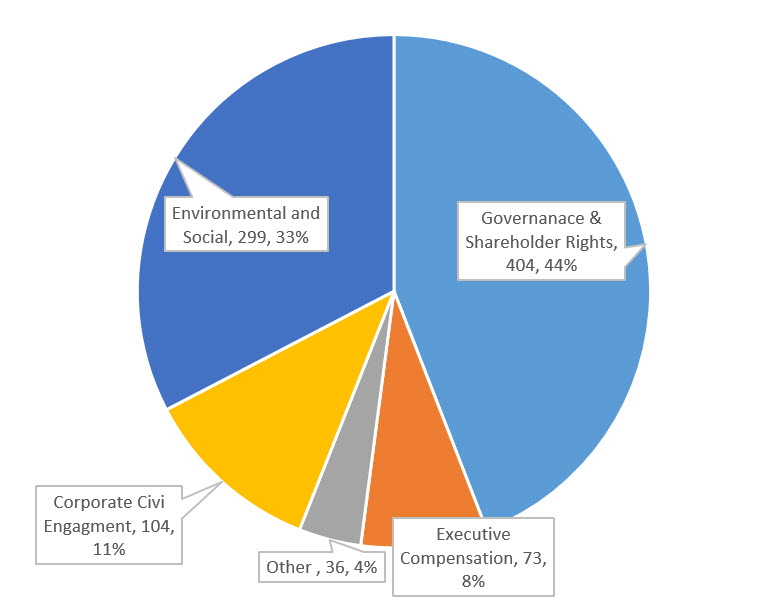

Shareholder advocacy and issuer engagement, which leverage the power of stock ownership in publicly listed companies, are action oriented approaches that rely on influencing corporate behavior through direct corporate engagement, filing shareholder proposals and proxy voting. These approaches have been employed more extensively in recent years to promote environmental, social and governance (ESG) agendas that may typically extend beyond an organization’s generally adopted guidelines and procedures governing proxy voting. Indeed, for the second year in a row through the 2016 shareholder meeting season, governance and shareholder rights proposals were the most frequently submitted shareholder proposals, according to Gibson Dunn. (refer to Exhibit 1). At the same time, shareholder proposals covering environmental and social issues, which received a boost in 2015 in the lead up to and adoption of the United Nations Framework Convention on Climate Change (otherwise referred to as the Paris Climate Agreement) and resultants commitments to reduce greenhouse gas emissions, attracted the second largest number of shareholder proposals in 2015 and again in 2016.

Exhibit 1: 2016 Shareholder Proposals by Issue

Source: Gibson Dunn

Bond owners, on the other hand, have adapted these approaches to focus on securing additional information and communicating by means of a direct dialogue on ESG related issues with management to influence issuer behavior, including companies, sovereigns and municipal entities, or modifying bond indenture terms and conditions. While bond ownership limits the advocacy options available to investors, such actions can extend beyond public companies to include privately held firms that tap the debt markets. This reach is not an available option for stockowners.

It should be noted that shareholder initiatives do not produce direct or near-term financial results but can lead to improved long-term performance aligned with changes to a company’s behavior and improved competitive positioning.

Equity Investors

Shareholders holding at least $2,000 worth of stock in a publicly-traded company for at least 1-year prior to a filing deadline can introduce a resolution to company management to be voted on at the next annual shareholder’s meeting. This has become an effective way of influencing company decision making and bring about corporate policy actions. The submission of a resolution creates an opportunity for a formal communication channel between shareholders and management that often results in the withdrawal of the resolution through a negotiated dialogue intended to addresses the concerns raised in the resolution. If an agreement is not reached, the resolution is placed on the company’s proxy statement and voted on by all shareholders. While the vast majority of shareholder proposals are non-binding, resolutions that attract a positive vote in excess of 10% are difficult for companies to ignore.

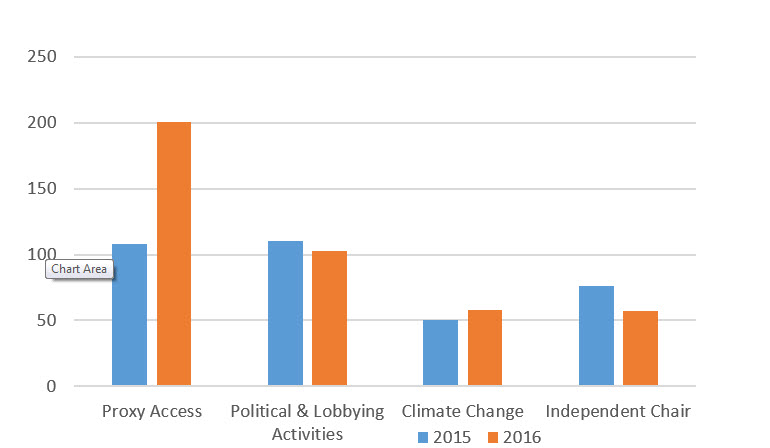

For example, during the 2016 proxy season, the most common shareholder proposal topic involved shareholder access, or actions by which shareholders sought to nominate their own director candidates to serve on the company’s board of directors. However, political and lobbying, advocacy for the establishment of an independent chair on a company’s Board of Directors and climate change were the next most common shareholder proposal topics. (refer to Exhibit 2). In turn, climate change proposals included reporting on climate change, greenhouse gas emissions and climate change action.

Exhibit 2: Most Common Shareholder Proposals 2015 – 2016

Source: Gibson Dunn

By purchasing shares of a company, an individual or institution, including a mutual fund becomes a shareholder of that company. For example, the New York Stock Exchange requires that companies listed on its exchange hold an annual meeting. Shareholders are invited to attend the meeting in person – or by proxy – to vote on issues brought before the meeting by the company or by other shareholders. Since attending the meeting is very likely inconvenient, most shareholders send in their proxies indicating how they would like to vote. Examples of issues that might be included in a proxy ballot are election of the Board of Directors, executive compensation packages, and approval of mergers or acquisitions

Proxy Voting

Proxy voting is the right of shareholders to vote their shares on corporate resolutions and in this way influence a company’s policies, practices and governance. Typical issues that might be included in a proxy ballot are the election of the Board of Directors, selection of audit firms, executive compensation packages, and approval of mergers or acquisitions.

The proxy voting guidelines cover a variety of issues, including the size and composition of Boards of Directors, independence of the Boards, executive compensation policies, changes in a company’s capitalization such as share issuance and repurchases, mergers and acquisitions, and situations unique to non-U.S. companies.

For example, the subject of board diversity, including gender and racial diversity, has been gaining attention in recent years. One large shareholder, State Street Global Advisors, has recently launched an initiative to pressure large companies to improve gender diversity on their boards by voting against the re-election of committee heads who do not prioritize the hiring of female directors. Of companies in the Russell 3000 index, almost 25% have no female board members, while 58% have boards that are less than 15% female, according to Institutional Shareholder Services reports.

Fixed Income

In the absence of an ownership relationship when investing in fixed income securities (unlike their ownership stake in a company via their shareholdings, bond investors are lenders who do not enjoy ownership rights) bond investors have begun in the last few years to engage with company or issuer management teams in an effort to improve ESG-related business practices.