The Bottom Line: Sustainable ultra-short bond funds can serve to offset the expected lower income from money funds by offering a modestly higher yielding alternative.

Short-term interest rates are declining after two interest rate cuts so far this year

The Federal Reserve’s quarter-point interest rate cut this week and the September 18, 2024 larger than expected 50 basis points (bps) rate cut, the first interest rate cut in four years, has now taken the Fed funds rate to a 4.5% – 4.75% range. 3-month Treasury bill yields dropped from 4.90% on September 17th to 4.64% as of October 31st and 4.63% as of November 17th while 10-year Treasury yields shifted higher, gaining 16 basis points from 3.6% to 3.81% on September 30th and 63 basis points by the end of October (perhaps indicating that investors may be concerned about rising government debt levels and the possibility of higher inflation ahead). The Fed signaled a more cautious note on Thursday about how quickly it may continue to lower rates. Before its action, however, 111 economists surveyed in a recent Reuters poll (conducted prior to yesterday’s rate cut and Tuesday’s election) predicted that the Federal Reserve will cut its key interest rate by 25 basis points on November 7 and more than 90% predict another quarter-percentage point move in December. Against this backdrop, money market fund returns will decline from their present levels once currently held money market portfolio holdings begin to roll off. Prime money market fund returns generated an average of 38 basis points in September, 1.22% over the trailing three months and 5.01% during the previous twelve-month interval. At the end of November, these declined slightly to 37 bps, 1.18% and 4.95%, respectively.

Sustainable ultra-short bond funds could serve to offset the expected lower income streams from money funds

For sustainable investors, sustainable ultra-short bond funds can serve to offset the expected lower income streams from money funds and offer a modestly higher yielding alternative. Ultra-short bond funds offer higher yields compared to money market funds (for example, ultra-short bond funds returned an average of 6.17% over the trailing twelve months, or 1.16% higher than the average money market fund return), they provide more protection against interest rate risk compared to longer-term bonds, and these funds are relatively liquid, allowing investors to easily access their money at the end of the day or intraday for ETFs. At the same time, ultra-short bond funds carry more risk than money market funds, including credit and default risk, as well as duration risk (a measure of how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Duration can also be used to measure how sensitive the price of a bond or fixed-income portfolio is to changes in interest rates) and their prices, or net asset values, will fluctuate. As a result, investors face some level of risk for the loss of principal in the near term. In the end, choosing between money market funds and ultra-short bond funds depends on each investor’s risk tolerance, investment goals, and need for liquidity.

|

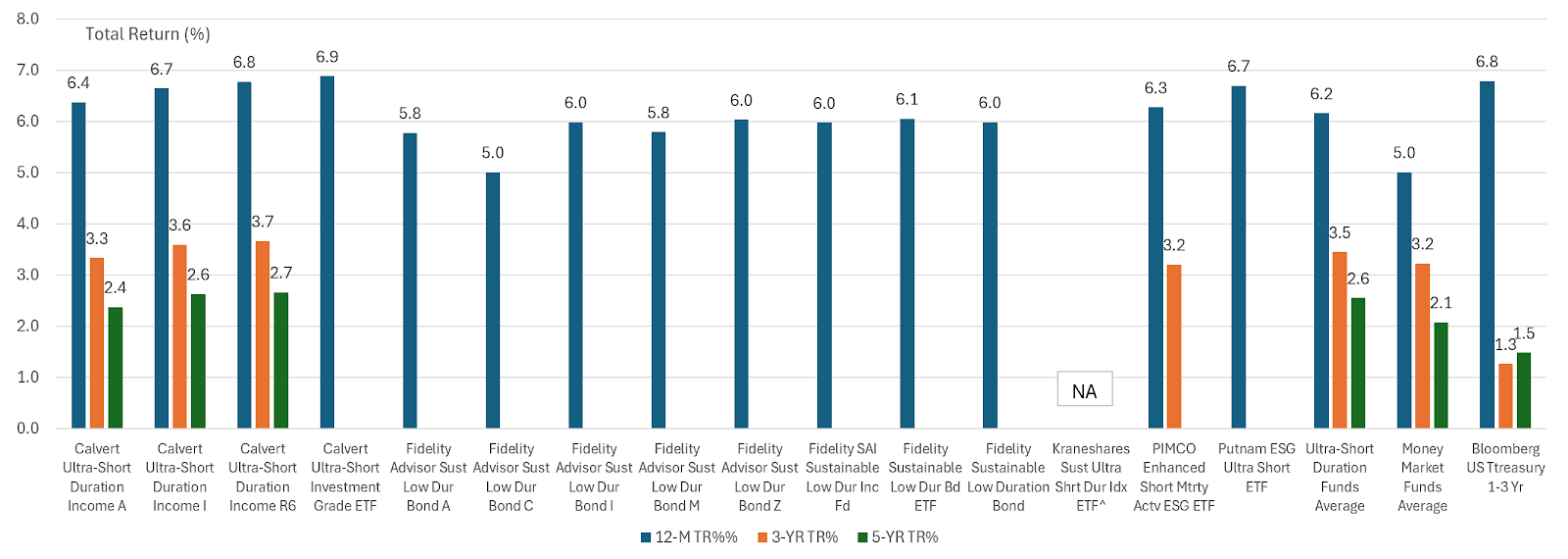

Performance (TR%) of sustainable ultra-short bond funds: 1-3-5 YRs to September 30, 2024 |

Notes of explanation: Funds listed in alphabetical order. ^=index tracking fund. Money market funds=prime funds. Sources: Morningstar Direct, fund prospectuses and Sustainable Research and Analysis LLC.

The universe of sustainable ultra-short bond funds offers investors some, but limited, options at this time

The universe of sustainable ultra-short funds is small, consisting of just six actively managed mutual funds and ETFs and only one passively managed ETF. The segment was recently expanded by one fund with the introduction on July 22, 2024 of the passively managed $300 million KraneShares Sustainable Ultra Short Index ETF (KCSH). The fund’s initial investments immediately pushed it to the number two spot in terms of assets under management, but some level of caution is advised. The fund’s initial investments may have been sourced to a single investor. If a redemption should occur unexpectedly, it could expose the remaining investors to unrealized losses and the fund’s closure.

Only two of the seven listed funds have been in existence long enough to establish three-year track records and only one fund, the $772.4 million Calvert Ultra-Short Duration Income Fund, has been in existence long enough to form a five-year track record. Launched in 2006, the fund dominates the $1.5 billion ultra-short segment, accounting for 52% of net assets.

The performance chart above covers the seven funds and related share classes, including index tracking and actively managed funds, arrayed in order of a Sustainable Research and Analysis scoring approach that ranks funds using a scale from A (Highest ranking) to D (Lowest ranking).

Only one fund, the actively managed Calvert Ultra-Short Duration Income Fund qualifies as the highest “A” ranked fund

Fund rankings, including index tracking and actively managed funds, are based on a screening and evaluation methodology that accounts for management company considerations, years in operations, fund size, performance track record and expense ratio. Based on this approach, the highest ranked fund, even after accounting for the fund’s relatively high expense ratios, is the Calvert Ultra-Short Duration Income Fund*.

This actively managed fund invests in dollar denominated investment-grade as well as non-investment grade (limited to 15%) corporate floating-rate securities and other debt securities. The fund maintains a portfolio duration of less than one year, and it pursues a four-fold sustainable investing strategy that incorporates the following approaches: (a) ESG integration. The portfolio manager(s) seek to invest in companies that manage environmental, social and governance (ESG) risk exposures adequately and that are not exposed to excessive ESG risk through their principal business activities. Companies are analyzed by the investment adviser’s ESG analysts utilizing The Calvert Principles for Responsible Investment (Principles), a framework for considering ESG factors (Refer to the Funds Directory tab for further details), (b) Screening. Through its Principles framework, Calvert seeks to identify companies and other issuers that operate in a manner consistent with or promote environmental sustainability and resource efficiency, equitable societies and respect for human rights and accountable governance and operations. (c) Exclusions. Certain issuers may be excluded from consideration, for example, manufacturers of tobacco products, and (d) Engagement. Active engagement with companies and other issuers, guided by Calvert’s Principles. Investors should evaluate the alignment of these sustainable approaches with their own sustainable preferences.

While Calvert has also been offering an actively managed ETF since January 2023 that pursues a similar sustainable investing approach and is subject to a lower 24 bps expense ratio, its fundamental investment strategy diverges in that its portfolio is restricted to investment-grade securities. Still, its rank suffers due to the absence of at least a three-year performance track record.

*Until December 2017 or so, the fund was called the Calvert Ultra-Short Income Fund and could invest up to 35%% of assets in non-investment grade securities versus the currently permitted 15%. This change, however, does not impact its 5-year performance track record.

Sustainable ultra-short bond funds: Assets, performance, expense ratios and rankings |

Fund Name | Net Assets ($ millions) | 12-M TR% | 3-YR TR% | 5-YR TR% | Expense Ratio (%) | Ranking |

Calvert Ultra-Short Duration Income A | 212.3 | 6.38 | 3.34 | 2.38 | 0.72 | A |

Calvert Ultra-Short Duration Income I | 483.5 | 6.65 | 3.6 | 2.63 | 0.47 | A |

Calvert Ultra-Short Duration Income R6 | 76.6 | 6.78 | 3.67 | 2.67 | 0.43 | A |

Calvert Ultra-Short Investment Grade ETF | 96.2 | 6.89 | 0.24 | B | ||

Fidelity Advisor Sust Low Dur Bond A | 4 | 5.78 | 0.45 | D | ||

Fidelity Advisor Sust Low Dur Bond C | 1 | 5.01 | 1.28 | D | ||

Fidelity Advisor Sust Low Dur Bond I | 0.7 | 5.99 | 0.25 | D | ||

Fidelity Advisor Sust Low Dur Bond M | 0.8 | 5.8 | 0.43 | D | ||

Fidelity Advisor Sust Low Dur Bond Z | 5.1 | 6.04 | 0.2 | C | ||

Fidelity SAI Sustainable Low Dur Inc Fund | 29.9 | 5.98 | 0.2 | C | ||

Fidelity Sustainable Low Dur Bd ETF | 3.8 | 6.06 | 0.2 | C | ||

Fidelity Sustainable Low Duration Bond | 17.5 | 5.99 | 0.25 | D | ||

Kraneshares Sust Ultra Shrt Dur Index ETF^ | 300 | 0.2 | C | |||

PIMCO Enhanced Short Maturity Active ESG ETF | 157.4 | 6.28 | 3.21 | 0.24 | B | |

Putnam ESG Ultra-short ETF | 102.7 | 6.7 | 0.25 | D | ||

Total/Average | 1,491.5 | 0.39 | ||||

Ultra-Short Duration Funds Average | 6.2 | 3 | 2.6 | |||

Prime Money Market Funds Average | 5 | 3.2 | 2.1 | |||

Bloomberg US Treasury 1-3 Yr | 6.8 | 1.3 | 1 |

Notes of explanation: Funds listed in alphabetical order. ^=index tracking fund. Annual and average annual performance to September 30, 2024. Rankings are on a scale from A (Highest ranking) to D (Lowest ranking). Data source: Morningstar Direct. Other sources: Fund prospectuses and Sustainable Research and Analysis LLC.