While not the first to deal with this subject, an article in the March 18, 2019 issue of InvestmentNews makes the case that even as demand for socially conscious investment products has never been greater “when it comes to the primary way in which younger generations invest through-company sponsored retirement savings plans, their desire to match their investments and values is falling on deaf ears.” In time, reluctance on the part of company sponsored plans to add ESG fund options is likely to be overcome, according to the article, in part, to attract talent by crafting benefit programs that appeal to today’s prospective employees, including ESG fund options in 401(k) plans. In addition to appealing to existing employees and plan participants, other reasons for adding ESG fund options include improved plan participation rates, potentially achieving positive societal impacts while at the same time contributing positively to long-term risk adjusted performance results. Still, a combination of issues could continue to restrict uptake, such as uncertainties surrounding the interpretation of fiduciary responsibility rules[1], legacy socially responsible performance concerns, the possible impact on overall plan administration costs, and the need for education. To these, the following should be added: (1) The trade-offs between adding one or more sustainable investment options[2] and a growing recognition that the simplification of and reduction in the number of investment choices leads to better participants experiences, (2) the challenge of satisfying the values orientation or sustainable investing sentiments of large and diversified participant populations with a single or a selected number of investment options, and (3) the limited number of sustainable fund options available at this time with track records that extend to three-to-five years. Taken together, even as more recent survey results point to some gains, these obstacles will likely continue to restrict progress around the adoption of sustainable investment choices in 401(k) plans. This article highlights these three considerations and a way forward around these.

Some progress regarding socially responsible investment choices in 401(k) plans

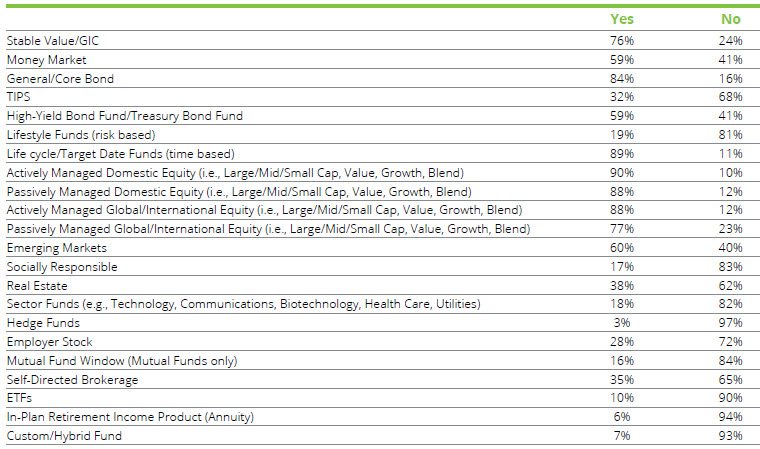

According to a Deloitte Consulting LLP Defined Contribution Benchmarking Survey, 2017 edition, while socially responsible fund offerings do not as yet appear in a listing of the top 10 offerings, the number of survey respondents offering socially responsible funds increased to 17% from 13% in 2015. Refer to Table 1. This is encouraging and contrasts with other, lower, estimates. For example, the article cited above notes that by most calculations less than 8% of company-sponsored retirement plans include even a single ESG fund option on the investment menu. Another source, the US SIF Foundation, based on an analysis of the holdings that 2,390 private sector retirement plans reported as of year-end 2014 to the Department of Labor found that less than 1% of the assets were invested in funds that explicitly market themselves as socially responsible investments (SRI). An earlier survey by the US SIF Foundation and Mercer, which specifically focused on sponsors of defined-contribution plans, found that while 14% of the 421 DC plan sponsors responding to the survey offered one or more SRI options, SRI options represented a low percentage of assets (around 1%).

Table 1: Responses to question-Types of investment options offered by your plan

Source: Deloitte Consulting LLP Defined Contribution Benchmarking Survey, 2017 edition, charting 240 plan sponsors

Admittedly, the comparison surveys are dated and survey results can diverge, in part, due to the use of varying survey methodologies and populations sampled. At the same time, and this is a larger issue, there is confusion and lack of uniformity around terms and definitions, not the least of which is the distinction between socially responsible investing and ESG integration.

After years of adding investment options to company sponsored 401(k) plans, especially following the introduction of life cycle/target date funds and their adoption as a default option, plan sponsors have begun to reverse course to focus instead on rationalizing and reducing the number of fund choices. This has been in response to research showing that too many investment fund choices tends to confuse plan participants and lead to sub-optimal investment decisions. Also, too much choice actually leads to lower plan participation rates. According to the same Deloitte survey, there has been a 13% decrease in investment options offered within retirement plans since 2015 and the average number of investment options offered is now below 20.

Trade-offs, limited availability of seasoned fund offerings and education have to be addressed

Against this backdrop, plan sponsors will be faced with having to assess the trade-off between adding a sustainable fund and, in the process, expanding the number of fund offerings or substituting a sustainable fund for an existing option. Substitution may not be a viable option and a related consideration is whether a single sustainable fund offering, such as an active or passively managed domestic equity fund (i.e. growth, value, large, mid or small cap), representing the most commonly available investment option, is sufficient to satisfy the sustainability objectives of large and/or diversified employee populations. Individual investors (as well as institutions) have varying opinions when it comes to their values and what matters most to them. It may be difficult to satisfy these with a single or even a complement of sustainable investment funds.

On top of that, a limited universe of recent vintage sustainable equity and fixed income funds are available at this time for evaluation as potential investment choices. It’s true that some sustainable funds have been in continuous operation since the early 1980’s, however, these are mainly socially responsible, values-based, funds that largely incorporate negative screening or exclusionary practices and/or these may be subject to higher fees. In contrast, more recently launched mutual funds and ETFs, both new funds and repurposed funds, that, for example, employ ESG integration practices, limited exclusions, and also engage in shareholder/bondholder advocacy complemented by proxy voting practices, have not as yet established track records that extend to three and five years. Such funds may not as yet qualify for consideration, thereby limiting the number of investment choices available at this time.

A way forward: Core equity offering, preceded by employee engagement and education

These challenges suggest that plan sponsors are likely to proceed with caution, and how to advance in the face of growing interest could be informed by seeking feedback from plan participants regarding their values and sustainability objectives. This can be accomplished by conducting employee roundtable or focus group discussions as well as employee surveys, both of which can also be used as a platform to educate employees regarding sustainable investing approaches and potential impacts. While the sustainable funds investment landscape is changing and more choices will continue to reach the market, one investment strategy that at present offers a more robust menu of investment choices, both actively and passively managed, is the blended large cap equity investment option. This investment choice can serve as a 401(k) plan’s initial supplemental entry into sustainable investing with limited disruption to the strategy of rationalizing the overall investment menu.

Once a decision has been made, plan sponsors will wish to further educate participants on the nature of the fund’s sustainable strategies, communicate expectations regarding the fund and its potential impacts and to offer periodic disclosures as to outcomes.

[1] Refer to 401(k) Plans and Sustainability Investing: Long-Term Companions, 2017

[2] Sustainable investment options refers to any investment choices that encapsulate one or more of the following approaches: values-based investing, negative screening or exclusions, thematic and impact investing, ESG integration, shareholder/bondholder engagement and proxy voting.