Sustainable Bottom Line: 92% of individual investors across three continents expressed an interest in sustainable investing, but the survey results also reveal issues/concerns that may lead to disenchantment.

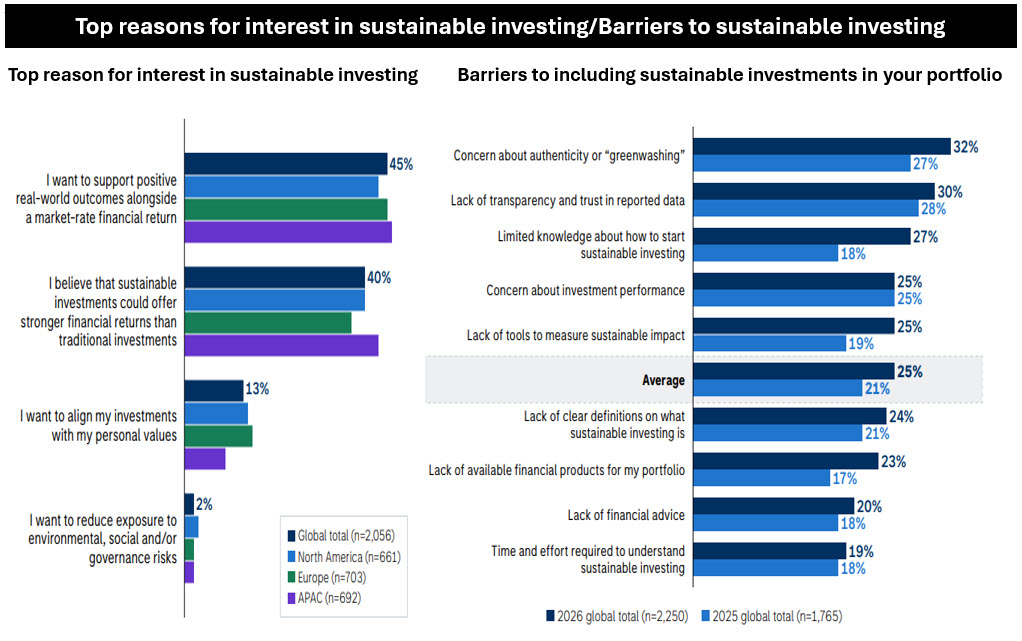

Notes of Explanation: Top reasons for interest in sustainable investing based on responses from those who selected very or somewhat interested in sustainable investing. Source: Morgan Stanley Institute for Sustainable Investing: How Individual Investors Are Approaching Sustainable Investing in 2026.

Notes of Explanation: Top reasons for interest in sustainable investing based on responses from those who selected very or somewhat interested in sustainable investing. Source: Morgan Stanley Institute for Sustainable Investing: How Individual Investors Are Approaching Sustainable Investing in 2026.

Observations:

• The April 23, 2026 dated Morgan Stanley Institute for Sustainable Investing Sustainable Signals report, How Individual Investors Are Approaching Sustainable Investing in 2026, reveals that sentiment in favor of sustainable investing on the part of individual investors remains strong globally. According to the report, 92% of individual investors across North America, Europe and Asia expressed an interest in sustainable investing.

• The survey, which included responses from 2,250 individual investors, indicates that expectations for financial returns continue to shape sustainable investment decisions, as performance remains the primary driver of both interest and allocation; and confidence in financial performance remains essential.

• According to the survey, about 45% of investors in the US who express a reason for interest in sustainable investing do so because they seek to support positive real-world outcomes alongside a market-rate financial return. Another 40% or so believe that they can achieve stronger financial returns than traditional investments. In addition, 64% say they plan to increase their allocation to sustainable investments over the next year, with 28% planning to maintain current levels and 5% expecting to decrease allocation.

• The survey also reveals several issues. Most notably, sustainable investment allocations have dipped from 33% to 31% in 2026. Also, across the average of 25% of 2026 respondents who rate a range of potential barriers to including sustainable investments as very significant, up four percentage points in the last year, greenwashing remains the leading worry among investors, with 32% citing it this year compared to 27% previously*. Additionally, 30% of participants expressed concerns about inadequate transparency and trust in reported data. Limited knowledge on how to begin sustainable investing was mentioned by 27%, while 25% each worry about investment performance and the absence of effective tools to assess sustainable impact.

• The survey defines sustainable investing for respondents as the practice of investing in companies or funds that “aim to achieve market-rate financial returns while considering positive social and/or environmental outcomes.” Yet 40% then said their top reason for interest was the belief that sustainable investments could offer stronger returns than traditional investments. This is in the face of limited evidence to support the idea that returns from sustainable funds** (other than perhaps selected thematic investments during certain market cycles) can exceed market-rate financial returns. That gap alone hints at expectation drift that isn’t grounded in either the survey’s own framing or in the empirical record, thus introducing a basis for future disenchantment with sustainable investing. Also, the other 45% of respondents seek to achieve “positive real-world outcomes alongside a market-rate return.” For investors relying on focused or labeled sustainable mutual funds and ETFs, such expectations may also lead to disenchantment (and bolster concerns about greenwashing) due to the fact that of the 522 dedicated funds at the end of March, few funds offer reporting that explicitly disclose non-financial outcomes. Further, the absence of clear standards, definitions, reporting and disclosure frameworks applicable to sustainable investing approaches and their outcomes contributes to the paucity of reporting on outcomes.

• To address these issues, it is necessary to enhance educational initiatives, raise standards, and step up transparency by strengthening reporting and disclosure frameworks.

* This level is even higher for institutional investors who in the most recent Sustainable Signals survey of institutional investors the average for very significant concerns rose to 38%, from 24% the year before.

**As used here sustainable investing is defined as indicated below.

Sustainable investing defined

While there is no universally accepted framework and definitions continue to evolve, today sustainable investing refers to a range of overarching investment approaches or strategies. That said, many practitioners agree that these approaches encompass the following strategies that may be employed individually or in combination:

Values-based investing. Also referred to as faith-based investing, socially responsible investing, responsible investing, ethical investing or investing based on a set of morals, the guiding principle is that investments are based on a set of beliefs with a view toward achieving a positive societal outcome. Typically, this approach is executed using exclusions as well as negative/positive screening.

Negative/positive screening or exclusionary strategies. Negative/positive screening is the process of identifying companies or other entities that score poorly or highly on environmental, social and governance (ESG) factors relative to their peers and underweighting or overweighting these in investment portfolios. On the other hand, an exclusionary strategy refers to the exclusions of companies or certain sectors from portfolios based on specific ethical, religious, social, environmental or governance guidelines or preferences. Traditional examples of exclusionary strategies cover the avoidance of any investments in companies that are fully or partially engaged in gambling and sex related activities, the production or manufacturing of alcohol, tobacco or firearms, or even atomic energy. These exclusionary categories have been extended in recent years to incorporate additional considerations, for example, firms that are the subject of serious labor-related actions or penalties by regulatory agencies or demonstrate a pattern of employing forced, compulsory or child labor, or firms that exhibit a pattern and practice of human rights violations or are directly complicit in human rights violations committed by governments or security forces, including those that are under US or international sanctions for grave human rights abuses, such as genocide and forced labor. That said, it should be noted that significant policy shifts and investor sentiment are taking place in North America and Europe regarding the treatment of nuclear energy and the defense sector, driven by recognition of nuclear energy’s role in meeting the dual goals of energy security and net zero emissions while the war in Ukraine has been responsible for shifting the perception and interest among institutional investors in the defense sector.

Closely related is the strategy of divestiture or divestment. Divestiture strategies involve current holdings that are liquidated over time as their eligibility is no longer consistent with the owner’s objectives, such as fossil fuel companies. But divestiture strategies may also involve a much broader universe of securities, such as when for example, divestiture strategies were applied to apartheid practices in South Africa in the 60s and 70s. At that time, any company doing business with South Africa was taken off the list of eligible investments.

Impact investing. Still a relatively small but growing slice of the sustainable investing segment, impact investments are incremental (additional) moneys directed to companies, organizations, and funds with the intention to achieve measurable social and environmental impacts alongside a financial return. Impact investments can be implemented in both emerging and developed markets and made across asset classes, such as equities, fixed income, venture capital, and private equity. In each instance, the objective is to direct capital to address challenges in sectors such as sustainable agriculture, renewable energy, conservation, microfinance, and affordable and accessible basic services, including housing, healthcare, and education.

Historically, impact investments have targeted a range of returns from below market to market rate, depending on the investors’ strategic goals. But increasingly, impact investing strategies are expected to at least achieve risk-adjusted market rates of return.

A more widely practiced yet less rigorous definition of impact investing involves providing direct exposure to issuers or projects that managers believe have the potential to achieve social or environmental benefits.

Thematic investing. An investment approach with a focus on a particular idea or unifying concept, for example securities or funds that invest in solar energy, wind energy, clean energy, clean tech and even gender diversity, to mention just a few of the leading sustainable investing fund themes. Investing in low carbon emitting stocks and bonds or green bonds or funds also fall into the thematic investing category. Funds classified under this category may or may not explicitly incorporate ESG factors in investment decision making.

ESG integration. This is a widely practiced (some data suggests the most widely practiced) investment approach by which environmental, social and governance factors and risks are systematically analyzed and, when these are deemed financially relevant and material to an entity’s performance, they will influence decisions on whether to buy or hold a security, and to what extent. Such considerations may lead to the liquidation of a security from the portfolio but at the same time, these factors may also identify investment opportunities.

Shareholder advocacy, issuer engagement and proxy voting. These strategies, which leverage the power of stock ownership in publicly listed companies and, regarding engagement, the power of bond investments, are action-oriented approaches that rely on learning about each company’s ESG practices and related risks and opportunities. These strategies also extend to influencing corporate behavior through direct corporate engagement, filing shareholder proposals and proxy voting.

Structural sustainability. The scope for expressing sustainability objectives through security selection or ownership rights in money market funds is inherently limited by regulatory requirements and liquidity mandates. As a result, many sustainable money market fund offerings pursue sustainability objectives through structural mechanisms that operate outside traditional portfolio construction, such as inclusive intermediation practices (e.g., broker-dealer selection and distribution partnerships) and the allocation of adviser revenues to charitable or social purposes. In this analysis, such approaches are characterized as forms of “structural sustainability,” reflecting their focus on market processes and economic flows rather than on portfolio composition or issuer engagement.

Updated 5/11/2026