Notes of Explanation: Companies stratified based on aggregate sustainability scores derived from publicly available information (e.g., sustainability reports, National Association of Insurance Commissioners (NAIC) filings, TCFD/ISSB disclosures, general account reporting, DC plan materials, and statutory statements. Methodology provides a disciplined approach for scoring providers on a 0–4 scale across seven categories and 30 subcategories, applying weights to reflect the materiality of each dimension, and producing an aggregate sustainability score along a range from 0 to 100. Sources: Publicly available information, Sustainable Research and Analysis LLC.

Observations:

• Vanguard Group announced on December 3, 2025, that it is developing a new target-date collective investment trust (CIT) series, Target Retirement Lifetime Income Trusts, that will allow older employees within 401(k) plans to shift some of their savings to buy annuities by incorporating the TIAA Secured Income Account as the lifetime income annuity option.

• Vanguard’s announcement underscores a broader market move of converting a portion of accumulated savings into guaranteed lifetime income inside defined contribution plans. By one estimate, over $100 billion is linked to Target Date Funds (TDA) with embedded guaranteed- income features. While insurers such as Prudential, TIAA, and BlackRock’s LifePath Paycheck Funds (which offer Group Annuity Contracts offered by one or more firms) have already introduced similar structures, Vanguard’s scale may accelerate adoption. The company manages about 40% of the $4.7 trillion in target date funds.

• The path to adoption will require that fiduciaries and sustainable investors, or their financial advisors, consider a framework for the purpose of evaluating group annuity contracts, both at the contract as well as contract provider level. Such a framework should likely consider not only investment-related environmental, social and governance (ESG) factors but also fiduciary governance, participant outcomes, product design, and long-dated balance-sheet risk management.

• A framework and evaluation methodology developed by Sustainable Research and Analysis that ensures transparency and replicability over time, by drawing exclusively from publicly available data, relies on seven broad categories and 30 underlying evaluation dimensions or subcategories. These factors include corporate & sustainability governance, retirement/Defined Contribution (DC) plan governance and fiduciary support, general/separate account investment practice, climate and environmental performance, in-plan annuity/DC product design, participant communications, social and inclusion outcomes, governance and business integrity.

• This methodology provides a disciplined approach for scoring group annuity providers on a 0–4 scale across the seven categories and 30 subcategories, applying weights to reflect the materiality of each dimension, and producing an aggregate sustainability score along a range from 0 to 100.

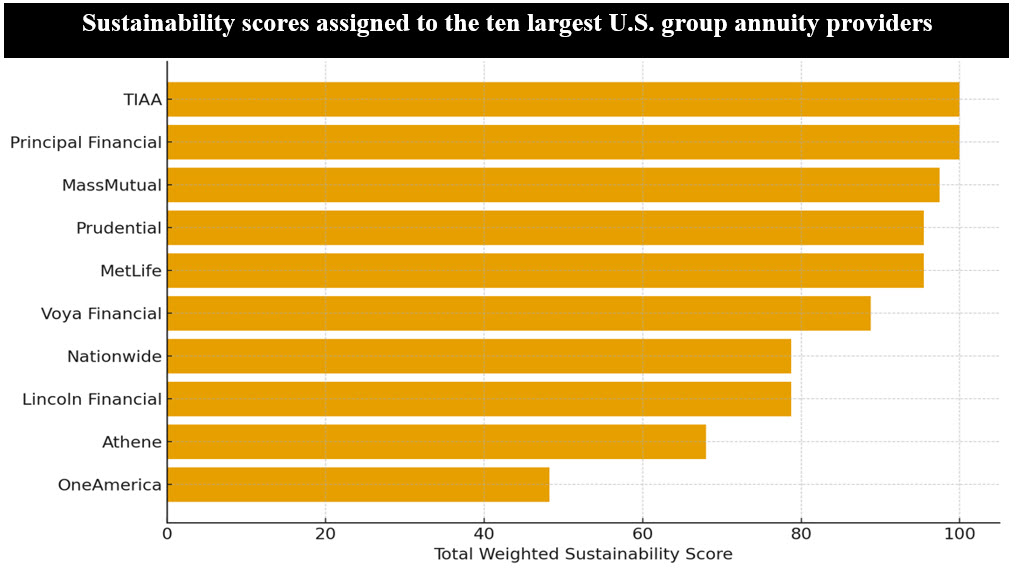

• The group annuity sustainability framework highlights a clear stratification among the ten largest U.S. group annuity providers by direct premiums written. While all are subject to broadly similar regulatory regimes and long-dated liability profiles, their approaches to sustainability, climate risk, and retirement-income design differ materially.

• According to this framework and methodology, TIAA, Principal Financial, MassMutual, Prudential, MetLife and Voya Financial form the leading cluster across most criteria. These firms tend to combine: (a) Formal board-level oversight of sustainability and climate risk, often through designated board committees or explicit governance mandates, together with executive accountability for ESG integration, (b) Mature disclosure practices, including sustainability or corporate responsibility reports aligned with Task Force on Climate-related Financial Disclosures (TCFD), the International Sustainability Standard Board (ISSB), or equivalent frameworks, and a growing focus on portfolio-level climate metrics, and (c) Well-developed DC and retirement platforms, where group annuity products are deliberately integrated into plan design, default strategies, and participant-income solutions (e.g., target-date funds, managed accounts, or guaranteed-income tiers).