Sustainable Bottom Line: SpaceX exclusion from the major US large-mid cap sustainable indices will have limited implications now but tracking deviations could widen over time.

SpaceX IPO: Record Scale, Constrained Float

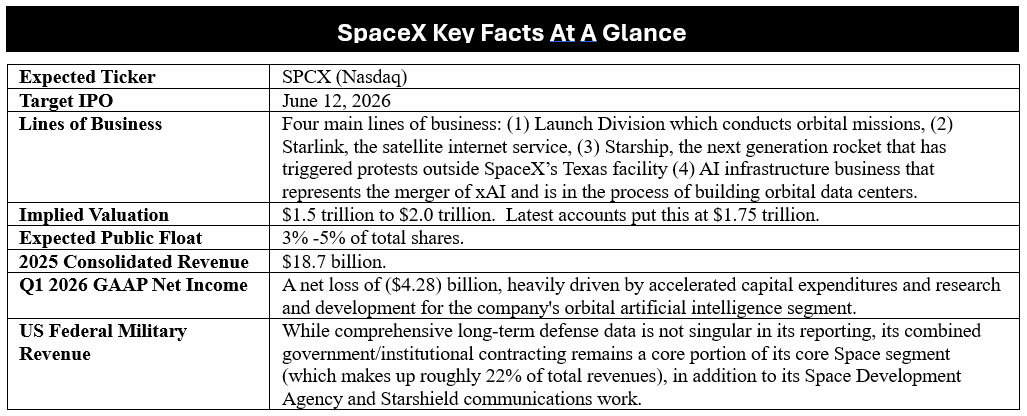

SpaceX is widely expected to complete the largest IPO in history on or about June 12, 2026, raising about $75 billion at a valuation of around $1.75 trillion–a level that some argue may be rich. The listing of the company will trigger accelerated inclusion into various conventional securities market indices, such as the Nasdaq-100 (Newly listed companies that rank in the top 40 of the Nasdaq-100 by market capitalization can now be added to the index after just 15 trading days, a drastic reduction from the previous minimum “seasoning” wait of three months) as well as other thematic indices, factor indices and widely followed broad-based indices, such as the MSCI USA Index, (typically effective after the 10th day of trading for mega-cap IPOs), the FTSE USA Index (now after just five days of public trading rather than the September or December 2026 reconstitution), and eventually the S&P 500 Index (S&P Global announced last week that it wouldn’t ease its index inclusion rules requiring companies that enter the S&P 500 to trade for a year and report profits across a span of four-quarters). That said, the initial SpaceX weight in broad-based indices is expected to be modest given the limited public float at inception, but it should grow over time as float increases. Modest float is not the likely case for broad-based sustainable indices that operate under fundamentally different eligibility criteria, including the three major US large-mid cap sustainable indices used by some of the largest sustainable index mutual funds and ETFs. These are the the FTSE US Choice Index (used by the $26.2 billion Vanguard Social Index Fund (VFTAX and VFTNA)), MSCI USA Extended ESG Focus Index (used by the $17.6 billion iShares ESG Aware MSCI USA ETF (ESGU)), and the S&P 500 Scored & Screened Index (used by the $2.8 billion Xtrackers S&P 500 Scored and Screened ETF (SNPE)). The first two benchmarks account for two-thirds of the labeled sustainable index funds market segment, measured by total net assets at the end of May 2026.

Unlike Tesla, a top 10 constituent in the Extended ESG Focus Index as well as the FTSE US Choice Index, but which is currently excluded from the S&P 500 Scored & Screened Index, SpaceX faces governance, environmental and social barriers that are likely to exclude the company from the three benchmarks in the near-term and perhaps beyond. However, sustainable investors who may still wish to gain exposure to the company through a mutual fund or ETF, while still preserving some level of sustainability in their overall portfolio, have several options to do so.

Notes of Explanation: Sources: Wall Street Journal, Barron’s, Sustainable Research and Analysis LLC

Notes of Explanation: Sources: Wall Street Journal, Barron’s, Sustainable Research and Analysis LLC

Sustainable indices screen stocks differently(1), using screens, exclusions and other conventions

Sustainable indices do not simply track the same universe as their conventional counterparts. They apply additional screens, exclusions, weighting conventions across certain companies, business activities and sectors, including severe and ongoing business controversies, ESG scores, as well as governance standards, that are specifically designed to exclude or minimize exposures to companies or industries whose operations or behavior fall below defined thresholds. The three indices examined here impose different methodologies, but SpaceX encounters listing obstacles under each. Here are some of the key considerations applicable to the three major US large-mid cap sustainable indices used in by some of the largest index tracking mutual funds and ETFs.

FTSE US Choice Index/Vanguard Social Index Fund

FTSE Russell issued a landmark announcement modifying its entire market protocol. It implemented a “Fast-Entry” mechanism that allows megacap IPOs exceeding a $13.5 billion threshold to bypass the standard quarterly waiting periods and enter the FTSE Global Equity Index Series and Russell US Indexes after just five days of public trading. It also granted a 12-month grace period on rigid lock-up and minimum free-float rules for top 500-sized IPOs, allowing SpaceX to clear immediate eligibility boundaries.

While SpaceX has been cleared for the standard Russell 1000 and FTSE All-World benchmarks, its inclusion in the sustainability-focused FTSE US Choice Index (formerly the FTSE4Good US Select Index) is highly uncertain due to the index’s core screening rules. These include, but are not limited to, the following:

–The Weapons Exclusion. The FTSE US Choice Index strictly excludes any companies involved in conventional or controversial military weapons. SpaceX holds deep, multi-billion dollar launch and satellite defense contracts with the U.S. military and Space Force (such as Starshield). Refer to the S&P 500 Scored and Screened Index for additional information.

–Corporate Conduct Audits. Once public, SpaceX will face immediate governance vetting under the UN Global Compact screen. Any unresolved labor or corporate governance disputes could trigger an automatic exclusion by the index committee.

-Corporate Governance. SpaceX’s IPO features a dual-class share structure that concentrates near-total voting control with Elon Musk. While FTSE Russell affords more latitude on multi-class structures than S&P Dow Jones, governance scoring is directly affected. Weak board independence and the absence of any ESG reporting infrastructure are additional negative signals.

-Labor Standards. Documented incidents at SpaceX Starbase, an industrial complex and rocker launch facility in Boca Chica, Texas, including welders working in closed, unventilated tents without respirators, multiple Occupational Safety and Health Administration (OSHA) investigations, and the dismissal of employees who organized internally, sit directly within FTSE’s labor standards assessment framework.

–ESG Disclosure History. FTSE’s ESG scores rely on publicly available data. As a private company for its entire existence to-date, SpaceX has published no ESG report, no emissions data, and no supply chain or human rights disclosures. The absence of this information handicaps any initial score.

MSCI USA Extended ESG Focus Index/iShares ESG Aware MSCI USA ETF

The MSCI USA Extended ESG Focus Index uses a strict optimization process that aims to maximize the overall ESG score of the index, as assigned by MSCI. It specifically selects companies based on their high ESG ratings per sector while deliberately keeping the index risk/return profile and sector weights extremely close to the parent index. The index enforces mandatory, broad business involvement exclusions. It specifically excludes companies involved in tobacco, controversial weapons, civilian firearms, thermal coal, and oil sands. Companies tied to serious environmental or social controversies are also excluded.

MSCI’s fast-track inclusion mechanism accelerates entry into the parent MSCI USA Index for qualifying mega-cap IPOs, but this mechanism operates at the parent index level, not within the ESG sub-indices. ESG-themed indices separately require an MSCI ESG Rating and an MSCI ESG Controversies Score, which SpaceX does not yet have. The implications are as follows:

-No Rating, No Entry. MSCI would need to initiate and complete a ratings assessment before SpaceX could be considered. Given the defense revenue profile, the absence of prior disclosures, the governance, environmental and labor controversies, achieving a rating of ‘BB’ or above, the typical threshold for top-50% sector selection, would be challenging in the near term. MSCI’s 2026 model update tightened several social and governance criteria, making a high initial score harder still.

S&P 500 Scored and Screened Index/Xtrackers S&P 500 Scored & Screened ETF

The S&P 500 Scored & Screened Index (formerly the S&P00 ESG Index) is constructed by removing a fixed set of business activity exclusions from the S&P 500 universe, then eliminating the bottom quartile of S&P Dow Jones Indices (S&P DJI) ESG-scored companies within each Global Industry Classification Standard (GICS) industry group. While other considerations may apply, SpaceX presents at least the following distinct challenges:

-ESG Score. The ESG scoring methodology relies on a bottom-up research process that evaluates up to 1,000 data points, with an emphasis on financial materiality and industry-specific criteria. As a newly public company with no history of mandatory ESG disclosure, SpaceX has no published S&P DJI ESG score. An absence of data typically results in a score at or near the sector floor, automatically placing the company at risk of falling into the bottom quartile. SpaceX’s governance structure (described below), environmental and ecological concerns surrounding its rocket launch activities and labor and workplace safety controversies documented over multiple years at its primary manufacturing facilities, such as OSHA violations at Boca Chica, Texas, are likely to weigh heavily in any initial assessment.

-Military Revenue Threshold. The index excludes companies deriving ≥10% of revenues from the manufacture of military weapon systems or “integral, tailor-made components.” SpaceX is reported to derive approximately 20% of its consolidated $18.7 billion in 2025 revenue from US federal and military sources, primarily NASA, the Department of Defense, Space Force, and the National Reconnaissance Office. Critically, the Starshield program, a dedicated classified military satellite network operated under a Department of Defense contract, blurs the line between launch services and tailored military systems. (Starshield is a dedicated business unit and satellite network adapted from Starlink, designed specifically for U.S. and allied government and military use. While Starlink provides consumer internet, Starshield focuses on national security by offering hardened communications, Earth observation, and hosted payload capabilities). Whether SpaceX’s Starshield program and defense launch contracts would be classified under these specific categories by S&P’s data provider is uncertain; launch services to military customers are not self-evidently weapons manufacturing. The more reliable near-term exclusion pathway is the ESG score screen, SpaceX’s absence of disclosure history would almost certainly place it in the bottom quartile of its sector peers.

Corporate Governance. Via the dual class structure, concentrates 80% of voting control in a single founder and limits shareholder accountability. A provision that would allow only Class B shareholders, meaning essentially Musk himself, to remove him as chief executive or chair. A mandatory arbitration clause for shareholder claims under US federal securities laws that would kill class action lawsuits entirely. And a reincorporation in Texas, where state law requires shareholders to hold 3% of outstanding stock to bring a derivative suit, the company’s high valuation sets up a high threshold as a very large number of shares will be required to challenge the board on anything.

-UN Global Compact (UNGC). The index excludes companies classified as non-compliant with UN Global Compact principles. The labor controversies cited above, and the summary dismissal of employees who raised concerns, would require examination under UNGC norms on labor rights and human rights.

Implications for sustainable index investors

As described, investors in broad-based sustainable index funds that track the MSCI USA Selection Index, the S&P 500 Scored & Screened Index or the FTSE US Choice Index will not gain automatic exposure to SpaceX following its listing, regardless of how large a position SpaceX becomes in the parent benchmark. Two of these indices, namely the MSCI USA Selection Index and the S&P 500 Scored & Screened Index, are constructed in a way that maintains the overall industry weights as their parent indices. This sector-neutral construction approach and fund expense ratios are likely the two most important factors in minimizing tracking error or the performance divergence historically associated with ESG screens, particularly underweighting energy. The FTSE US Choice Index is somewhat less prescriptively sector-constrained, yet this hasn’t diminished the capacity of the fund to maintain narrow annual deviations in the fund’s performance results. The absence of SpaceX or constrained initial weight is expected to dampen performance deviations relative to conventional counterparts in the near-term and such deviations are expected to be small. These performance deviations will widen, however, as SpaceX enters various indices and its weighting grows over time.

Options for sustainable investors

For sustainable investors who are comfortable with SpaceX’s exclusion from their universe, the position is clear: the index methodologies are doing precisely what they were designed to do. For those who are not, the SpaceX listing provides a sharper-than-usual illustration of the active decisions embedded in every passive ESG strategy.

Notwithstanding SpaceX’s ESG challenges, sustainable investors who still wish to gain exposure to the company through a mutual fund or ETF while still preserving some principle of sustainability may wish to consider one of the following approaches, or some variation of these approaches:

ESG Integration. The debates about active vs. passive investing aside, investors may wish to consider investing in an actively managed broad-based, style based (such as growth/value, large, mid and small cap) or thematic fund that employs an ESG integration strategy, either explicitly in the form of a labeled sustainable fund or as part of the investment management firm’s overall stewardship principles. The distinction between ESG exclusions and screening (which is what the three indices use) and ESG integration (where financially relevant and material ESG factors are inputs to valuation and risk assessment but not hard screens) is important and often poorly understood by investors. An active manager employing ESG integration could hold SpaceX at varying weights that account for the firm’s exposure to the governance, environmental and social risks as well as upside potential in its modeling of the firm’s valuation, rather than excluding it entirely. This is one of the most widely practiced sustainable investing approaches employed by institutional as well as retail investors worldwide. In effect, it says “I am pricing the ESG risk, not ignoring it.”

Reallocating part of a broader portfolio to gain SpaceX exposure through a conventional fund does not prevent an investor from continuing to hold a core sustainable index fund position.

Engagement as a strategy. For institutional investors large enough to make it credible, buying SpaceX post-IPO and then formally engaging management on ESG disclosure, labor practices, and governance is a legitimate sustainable investing pathway — the “own it and change it” philosophy that organizations like the Principles for Responsible Investment (PRI) and the Interfaith Center on Corporate Responsibility (ICCR) have long advocated. The dual-class structure limits voting leverage, but direct management engagement, coalition-building with other institutional holders, and public shareholder statements have moved companies with similar governance structures before.

The Starlink impact lens. While not a mainstream view, a smaller but real constituency of impact-oriented sustainable investors may actually view SpaceX positively rather than negatively. SpaceX’s Starlink’s mission of providing broadband connectivity to underserved and remote communities globally has a credible United Nations Sustainable Development Goals (SDG) SDG 9 (infrastructure and innovation) and SDG 10 (reduced inequalities) argument. For investors whose sustainable framework encompasses positive impact alongside exclusions, this lens could support holding SpaceX as a net-positive-impact company despite the defense revenue and governance concerns.

A watch-and-wait approach with defined trigger criteria. Some sustainable investors may find it useful to commit in advance to the conditions under which they would add SpaceX exposure, for example, publication of a first sustainability report, achievement of GAAP profitability, a reduction in military revenue concentration below a threshold, or structural governance reform. This is more principled than either permanent exclusion or unprincipled ad hoc buying, and it keeps the door open for inclusion without abandoning the ESG framework.

Sidebar: How the Largest Sustainable Index Funds Performed: 2021–2025

One of the most often discussed questions regarding sustainable investing is how sustainable investment funds perform relative to their conventional counterparts over time. In this context, a persistent theme has been that in sustainable investing ESG screening and exclusions impose a meaningful performance penalty. While this may be the case under some scenarios involving sustainable investing approaches, it doesn’t address the more nuanced landscape of sustainable investing more broadly—one that involves at least seven broad approaches to sustainable investing along with various gradations. These include values based investing, negative/positive screening or exclusionary strategies, impact investing, thematic investing, ESG integration, shareholder advocacy, issuer engagement and proxy voting, and structural sustainability. Each of these approaches, applied individually or in some combination, may produce varying performance results. In addition, significant differences around ESG scoring and ESG scores, the shifting sustainable strategies by funds over time, limited investment track records, and a more constrained number of labeled sustainable fund categories relative to conventional funds, are some of the reasons that it has been challenging to resolve the performance related questions.

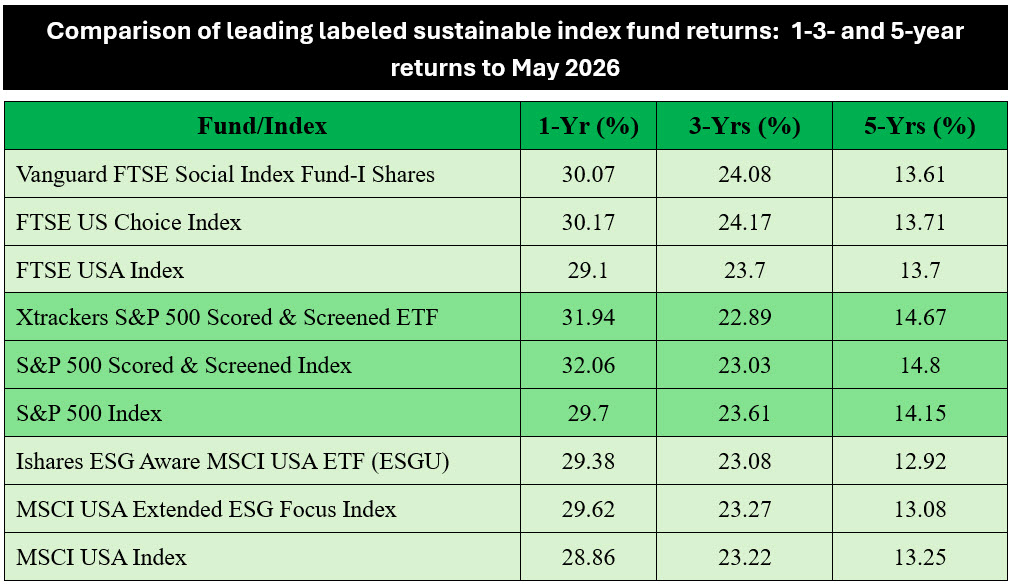

That said, a review of the performance track record of the three large broad-based labeled sustainable index funds that employ a combination of similar (but not identical) screening, exclusions and weighting conventions while attempting to achieve sector neutral approaches (in the case of two of the funds) shows that the three funds tracked their conventional counterparts with a degree of high closeness while exhibiting modest and alternating outperformance and underperformance across individual years.

Of the three funds, none experienced any negative performance deviations over the course of one-year in 2025. The widest negative deviation was recorded by the Xtrackers S&P 500 Scored & Screened ETF over the three-year interval when the fund underperformed the conventional S&P 500 Index by an average annual 72 basis points. When the three-year interval is extended to five years, the fund outperformed its conventional index by 52 basis points. The best track record of the three funds has been achieved by the Vanguard FTSE Social Index Fund Institutional Shares. The fund underperformed the FTSE USA Index over the trailing five years by a very narrow average annual 9 basis points, a tracking error that can largely be accounted for by the fund’s expense ratio that has declined over time. Unlike the two other funds, the FTSE Social Index Fund does not employ a sector neutral construction approach.

Notes of Explanation: Three-and five-year returns are average annual rates of return. The Vanguard FTSE Social Index Fund I Shares expense ratio declined from 12 basis points at the end of 2021 to 3 basis points today. Sources: Morningstar, MSCI, FTSE and S&P Dow Jones Indices.

Notes of Explanation: Three-and five-year returns are average annual rates of return. The Vanguard FTSE Social Index Fund I Shares expense ratio declined from 12 basis points at the end of 2021 to 3 basis points today. Sources: Morningstar, MSCI, FTSE and S&P Dow Jones Indices.

The strong five-year performance track record of the three ESG indices shows that the methodology works, and SpaceX’s exclusion is unlikely to disrupt that in the near-term, though the medium-term trajectory bears watching.