The Bottom Line: SEC Asset Management Advisory subcommittee introduced preliminary set of potential ESG investment product reporting and disclosure recommendations at December 1, 2020 meeting.

SEC subcommittee introduced preliminary set of potential ESG investment product reporting and disclosure recommendations

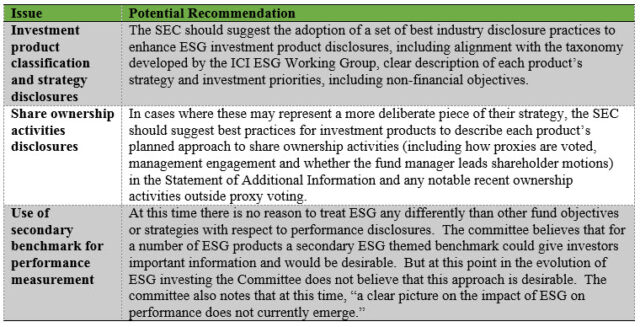

At the December 1, 2020 SEC meeting the ESG subcommittee of the Asset Management Advisory Committee (AMAC) introduced a preliminary set of potential reporting and disclosure recommendations that would apply broadly to issuer ESG disclosures as well as to ESG investment product disclosures. The purpose is to arrive at final recommendations for consideration by the SEC at the next subsequent AMAC meeting, the date for which has not as yet been posted on the SEC’s website. In the area of investment product disclosures that would cover mutual funds and ETFs, the subcommittee outlined three preliminary proposals designed to foster greater disclosure, transparency and comparability regarding ESG fund practices, including alignment with the recently published taxonomy developed by the ICI ESG Working Group. The subcommittee’s preliminary set of potential reporting and disclosure recommendations represent a much needed step forward in addressing growing confusion and increasingly common misunderstandings on the part of stakeholders between values-based investing and environmental, social and governance (ESG) integration and expectations regarding their financial and non-financial outcomes. At the same time, the ICI’s ESG Roadmap, if it is to be taken up formally by the SEC, should be viewed as a good starting point that still requires additional consideration and further refinements before final adoption to achieve greater clarity regarding terminology and practices across the growing universe of sustainable investment funds.

ESG investment product reporting and disclosure recommendations

The following is a snapshot of the three tentative proposals and recommendations being considered by the SEC’s ESG subcommittee of the Asset Management Advisory Committee:

According to a prepared discussion draft document, the subcommittee noted that the committee was formed in the first quarter of 2020 with the purpose of looking into ESG practices in investment products and to “explore, within the areas of the SEC’s mandate, whether any recommendations were warranted to improve practices.” This was initiated against a backdrop of significant ESG investing growth in recent years that the committee noted, based on ICI data at the time, runs to 1,102 products and $1.7 trillion in assets under management at the end of June 2020.

Observations

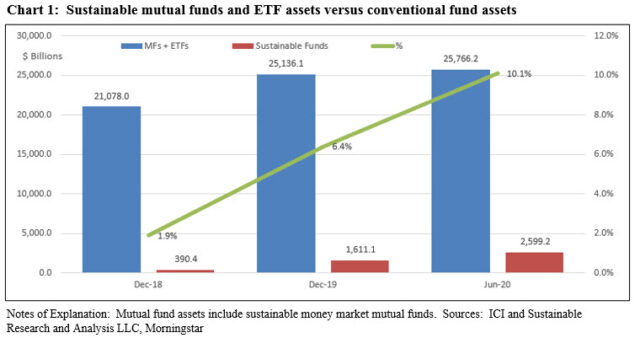

The growth in the number of investment management firms offering sustainable mutual funds and ETFs and the rapid expansion in the number of funds as well as assets under management as of June 30 of this year far exceeds the numbers attributed to the ICI. According to research conducted by Sustainable Research and Analysis LLC based on widely accepted sustainable investing definitions[1], 182 separate firms were offering a total of 4,534 sustainable funds/share classes and ETFs with combined assets that reached $2.6 trillion at the end of June 30, 2020, up from $390 billion at the end of 2018. The growth in AUM, which more recently reached around $2.8 trillion, is almost entirely attributable to fund re-brandings and to a lesser extent, market movement and positive fund flows. In just a short 18-month period, sustainable mutual funds and ETFs jumped from 1.9% of industry assets at the end of 2018 to 6.41% at the end of 2019 and to 10.1% as of June 30, 2020. This is the first time sustainable fund assets exceeded 10% or more of fund industry assets. Refer to Chart 1.

Regardless of the number, what has been clear is that the evolving nature and expansion of the sustainable funds segment without a common set of definitions applicable to the various sustainable investing terms and portfolio management approaches seem to correlate with growing confusion and an increasingly common misunderstanding on the part of stakeholders between values-based investing, reflecting social or ethical investing considerations, and environmental, social and governance (ESG) integration, pursuant to which relevant and material risks and opportunities are taken into account in the process of evaluating securities. To ensure continued growth and development in the sustainable investing sector and to allow it to reach its full potential, Cosack and Shilling in a paper published earlier this year[2] proposed three key standard setting recommendations for consideration and debate. These recommendations include the adoption of standardized sustainable investing strategy definitions, creation of a generally accepted mutual fund/ETF product classification framework and stepped up fund disclosures practices. The SEC’s preliminary proposed reporting and disclosure recommendations align in their sentiments with three key proposed standard setting recommendations advanced by Michael Cosack and Henry Shilling.

The ICI ESG Roadmap embraces two principles: Use of a consistent framework for classifying and describing funds and the adoption of these in public communications

The ICI ESG Roadmap embraces two principles. First, is the introduction of a consistent framework to cover the various ESG and sustainable investing approaches, using the following three nonexclusive approaches as set forth in the ESG Roadmap:

-

- ESG exclusionary investing:Funds using an ESG exclusionary investing approach may exclude companies or sectors that do not meet certain sustainability criteria or do not align with investors’ objectives. For example, a fund may not invest in companies that have significant business related to weapons manufacturing or distribution, gambling, tobacco, alcohol, or nuclear energy.

- ESG inclusionary investing:Funds using an ESG inclusionary investing approach generally seek positive sustainability-related outcomes by pursuing and focusing on portfolios that fundamentally or systematically tilt a portfolio based on ESG factors alongside financial return. For example, a fund may invest in equity securities of companies that contribute to and benefit from clean energy generation, sustainable infrastructure, waste management, and other environmentally friendly approaches.

- Impact investing:Funds using an impact investing approach seek to generate positive, measurable, and reportable social and environmental impact alongside a financial return. Measurement, management, and reporting of impact is a defining feature of impact investing. For example, a fund may invest the majority of its assets in securities whose use of proceeds, in the fund manager’s opinion, provide measurable positive social or environmental benefits.

The second principle is to incorporate the agreed up common terminology into public communications describing ESG integration and sustainable investment strategies.

The ICI’s ESG Roadmap, if it is to be taken up formally by the SEC, should be viewed as a good first step forward in a process that in our view will require additional consideration and further refinements to achieve greater clarity regarding terminology and practices across the growing universe of sustainable investment funds. For example, the ICI’s ESG Roadmap does not address the adoption of standardized sustainable investing definitions, and related to this, the financial and non-financial expectations or outcomes associated with funds that pursue such strategies. Also, the ICI’s investing approaches do not fully differentiate between various types of funds and their sustainable strategies, such as thematic or values-based funds. Addressing these considerations would serve to further support financial intermediaries and investors in their efforts to more effectively align funds with sustainable goals, objectives or values. While the ESG Roadmap does not offer any guidance regarding stepped up disclosure practices that help investors understand the relationship between the adoption of sustainable strategies, how such strategies may be impacting investment decisions as well as financial and, as relevant and appropriate, non-financial outcomes, this shortcoming seems to be addressed in the broader set of subcommittee’s recommendations.

[1] While definitions continue to evolve, sustainable investing refers to a range of five overarching investing approaches or strategies that encompass: values-based investing, negative screening (exclusions), thematic and impact investing and ESG integration. Shareholder/bondholder engagement and proxy voting may also be employed along with one of more of these strategies that are not mutually exclusive.

[2]Promoting the Continued Growth and Development of Sustainable Investing in US Mutual Funds and ETFs: A Three-pronged Proposal to Address Misunderstanding and Confusion that Have Arisen in the Sector, Michael Cosack and Henry Shilling, May 2020.