Sustainable Bottom Line: The 15 focused sustainable taxable bond fund categories delivered a tale of sharp short-term pain against a backdrop of still-intact longer-term gains.

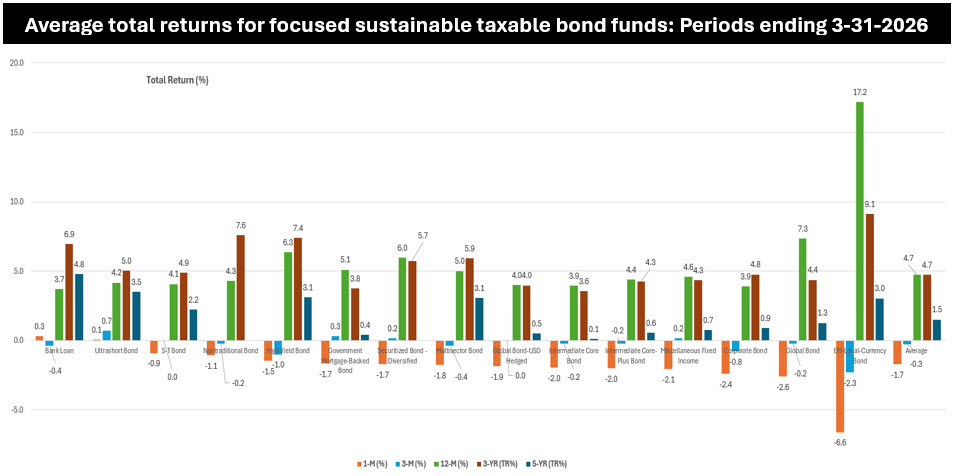

Notes of Explanation: 15 labeled sustainable taxable bond fund categories as classified by Morningstar/ Categories listed in descending order, based on March 2026 average total return results. Sources: Morningstar and Sustainable Research and Analysis LLC.

Notes of Explanation: 15 labeled sustainable taxable bond fund categories as classified by Morningstar/ Categories listed in descending order, based on March 2026 average total return results. Sources: Morningstar and Sustainable Research and Analysis LLC.

Observations:

• Turbulence in March wiped out year-to-date gains. The average gains recorded in the first two months of the year by the universe of labeled sustainable taxable fixed income funds were offset in March, to end the quarter in the red. Still, 12-month returns remained broadly intact. Consisting of 15 sustainable taxable bond fund categories based on tracking by Morningstar, across some 210 funds/share classes, including ETFs, and representing approximately $41.3 billion in assets under management (AUM), the taxable segment delivered a tale of sharp short-term pain against a backdrop of still-intact longer-term gains. Municipal bond funds were not spared.

• The Iran conflict was the defining macro shock of March. U.S and Iran hostilities erupted at the end of February, triggering the closure of the Strait of Hormuz and what the IEA called the largest oil supply disruption in market history. The resulting energy-price surge drove TIPS breakeven rates to near one-year highs, forced a hawkish repricing of Fed rate-cut expectations, and produced a classic bear-flattening of the yield curve, with the 10-year Treasury rates hitting 4.30% on March 31, down from 4.44% a few days earlier, their highest in 2026. These shocks compounded pre-existing headwinds of persistent inflation, trade-policy uncertainty, and softening labor-market data.

• March and Q1 returns were broadly negative, but short-duration categories held up. Thirteen of 15 categories posted negative 1-month average returns (simple average: −1.7%). Emerging Markets (EM) Local-Currency Bond funds were hardest hit (−6.6%), followed by Global Bonds (−2.6%) and Corporate Bonds (−2.4%). Only Bank Loan funds (+0.3%) and Ultrashort Bond funds (+0.06%) finished March positive, their floating-rate and low-duration structures providing a natural buffer against rate volatility. For the first quarter as a whole, the simple average return was −0.3%.

• Every category remained positive over the trailing 12 months. Despite first quarter turbulence, all 15 categories delivered positive average total returns through March 31, 2026 (simple avg: +5.0%). EM Local-Currency Bond funds led at +17.2%, followed by Global Bond funds (+7.3%) and High Yield (+6.3%). The two largest categories by AUM, Intermediate Core Bond funds ($17.2B, +3.9%) and Intermediate Core-Plus Bond funds ($8.8B, +4.4%), anchored the aggregate result with modest but meaningful positive real returns.

• Multi-year returns still carry the scar tissue of the 2022 rate shock. Three- and five-year averages remain mixed. Higher-octane categories lead the 3-year rankings, EM Local-Currency funds (+9.1%), Nontraditional Bond funds (+7.6%), and High Yield (+7.4%), while core investment-grade categories remain depressed. Intermediate Core Bond funds’ 5-year average of just +0.1% and Corporate Bond funds’+0.9% illustrate how deeply the 2022 rate shock cut into compounded long-term returns.

• Floating-rate and ultrashort strategies have been the standout multi-cycle performers. Bank Loan funds (+4.8% 5-yr avg.) and Ultrashort Bond funds (+3.5%) rank among the strongest performers across the full five-year window, rewarding investors who maintained low-duration exposure through both the 2022 rate spike and the more recent Iran-driven volatility. Their March resilience reinforces this pattern.

• What This Means for Investors. Investors shouldn’t overreact to short-term losses. The March and first quarter drawdowns are real but so far contained. With all 15 categories still positive over 12 months, the longer-term case for conventional as well as sustainable fixed income remains intact. Repositioning in response to a single month’s volatility risks locking in losses. Still, investors might reassess duration risk considering geopolitical volatility, consider floating-rate/ultrashort as a tactical buffer and monitor EM Local-Currency closely given the category’s extreme returns dispersion.