Vanguard Shareholders Vote on Genocide-Free Investing in Mutual Funds

Today Vanguard is holding a Joint Special Meeting of Shareholders in Scottsdale, Arizona. Shareholders have been asked to vote on board of trustees nominations and on several fund proposals that will harmonize policies across Vanguard’s US-based funds. In addition, Vanguard shareholders have had the opportunity to vote on a proposal spearheaded by Investors Against Genocide (IAG), a citizen-led initiative dedicated to convincing mutual funds and other investment firms to make an ongoing commitment to genocide-free investing. The proposal calls upon Vanguard to institute transparent procedures to avoid holding investments in companies that, in management’s judgement, substantially contribute to genocide or crimes against humanity, the most egregious violations of human rights. While its sentiment extends beyond Sudan, IAG is advocating in particular for targeted divestiture from companies that support government-sponsored genocide in Sudan, specifically identifying four foreign oil companies, including one with two publicly traded subsidiaries and two with ADRs listed in the US, that are the largest business partners with the government of Sudan. These firms, five in total, each of which is domiciled in a developing market, are: China Petroleum & Chemical Corporation/Sinopec and PetroChina/CNP, both China based, ONGC of India and Malaysia-based Petroliam Nasional Berhad (PETRONAS) via its two publicly listed subsidiaries. The resolution, as it relates to Sudan, is not likely to have an impact on Vanguard’s funds with a US focus. Affected mutual funds are more likely to be actively managed equity and bond funds as well as index funds with a global mandate that include developing markets, emerging markets and Asia-Pacific region, in particular, as well as global bond funds. That said, passage is unlikely. Vanguard acknowledges that the humanitarian issues on which this proposal is ultimately focused are of consequence and deep concern, however, Vanguard opposes the resolution for at least four reasons.

Vanguard is the second largest asset management firm in the world with about $4 trillion in assets under management, offering 180 funds and serving over 20 million investors worldwide. It stands to reason that a large number of investors in some of Vanguard’s index funds are likely to be impacted but concerned investors always have the option to vote with their feet, if they wish, by exiting from funds that currently hold such securities and/or funds that have the guidelines flexibility to do so currently or in the future. That said, there are limited alternative investment options within Vanguard itself as the management company only offers one US focused sustainable investment fund[1]. On the other hand, investors with flexibility to invest outside of Vanguard’s universe of 180 investment funds can pivot into mutual funds with similar investment objectives but which, at the same time, explicitly integrate environmental, social and governance (ESG) strategies that are more likely to exclude firms engaged in genocide or do business in the Sudan. Some funds in this category, but not all, also specifically exclude funds doing business in Sudan. There are at least 10 actively managed equity funds and two actively managed bond funds as well as just two index mutual funds, all outside of the Vanguard complex, available as potential investment options for investors[2]. While these are listed below, investors should be cautioned that, as is the case before investing in funds more generally, due diligence should be conducted to ensure that, at minimum, these funds satisfy basic requirements, including qualifications and skills to combine financial and sustainability characteristics, a demonstrated, established and consistent performance track record over time, properly sized funds for scale and liquidity and effectively priced fund offerings. In a future article, these funds will be more formally evaluated.

Sudan’s Genocide Has Been Going On for Decades

In one of the worst campaigns of violence and mass slaughter since World War II, it has been reported that more than 2.5 million civilians have been killed in Sudan over decades of brutal conflict between north and south, in Darfur in the west, and in other regions of Sudan.Since the 1950s, the Arab-dominated government of Sudan, centered in the capital Khartoum and led by President Omar al-Bashir who came to power in a 1989 coup, tried to impose its control on the country’s African minorities living along the nation’s periphery. The result has been a deadly mix of ethnic, religious, politically motivated and, since the discovery of oil in the South in 1973, financially fueled conflicts.Though the north-south civil war ended in 2005 when, under heavy international influence, a Comprehensive Peace Agreement was signed and South Sudan gained its independence in July 2011, systematic violence has continued.

In 2003, the Sudan government responded with crushing brutality to a rebellion in the Darfur region of Sudan, beginning a genocidal campaign against civilians that resulted in the deaths of nearly 400,000 people, the systematic raping of women, the burning of villages, the poisoning of wells and the displacement of millions of people that by some estimates exceed three million. Both the African Union and the United Nations introduced forces to stop the violence and assist the internally and externally displaced refugees.

The situation in Sudan is not disputed. The United States, under President Clinton, first imposed sanctions on Sudan in 1997, including a trade embargo and blocking government assets, in response to the Sudan’s government support of international terrorism, ongoing efforts to destabilize neighboring governments, and the prevalence of human rights violations, including slavery and the denial of religious freedom. Additional sanctions were added in 2006 in response to the persistence of violence in Sudan’s Darfur region, particularly “against civilians and including sexual violence against women and girls, and by the deterioration of the security situation and its negative impact on humanitarian assistance efforts.[3]”

Even before its embargo extension, the United States government in 2004 recognized the actions of the Sudanese government as genocide under the United Nations (UN) Genocide Convention.

Shortly thereafter, in March 2005, the UN Security Council referred the case of Darfur to the International Criminal Court (ICC). On March 4, 2009, the ICC announced a historic decision to issue an arrest warrant charging Sudanese President Bashir with five counts of crimes against humanity and two counts of war crimes for his leadership role in orchestrating the conflict in Darfur. Despite his indictment, President Bashir remains in office and travels abroad with impunity, as do other Sudanese leaders charged with war crimes and crimes against humanity.

While the conflict has faded from the spotlight, ongoing violence continues to displace, injure, and kill people today. According to the Human Rights Watch 2017 World Report, Sudan’s human rights record remains abysmal in 2016, with continuing attacks on civilians by government forces in Darfur, Southern Kordofan, and Blue Nile states; repression of civil society groups and independent media; and widespread arbitrary detentions of activists, students, and protesters. The ruling National Congress Party proceeded with a national dialogue process to pave the way for a new constitution and government, following the independence of South Sudan, despite a boycott by several opposition parties.

Still, after temporarily easing sanctions in January of this year, the US last month permanently lifted a raft of sanctions on Sudan, saying the African nation had begun addressing concerns about terrorism as well as human rights abuses against civilians in the country’s Darfur region. The decision to lift the sanctions and end an economic embargo comes after the Trump administration last month removed Sudan from the list of countries whose citizens are subject to travel restrictions. Sudan was the only country that was removed.

Following the civil war, the genocide and the 1997 imposition of a comprehensive trade embargo by the US against Sudan, US companies and many international petroleum companies withdrew from the Sudanese market, but some foreign companies continue to do business in Sudan.

The Investors Against Genocide (IAG) Case

Investors Against Genocide was founded in 2006 to advocate for targeted disinvestment from companies that supported the genocidal regime in Sudan. While US companies and many international companies had exited the Sudanese market following the imposition in 1997 of a comprehensive trade embargo against the Sudanese government, IAG advocates for investment firms to avoid or divest their holdings in four foreign oil companies that are significant business partners with the Government of Sudan. These companies are large energy companies headquartered in the emerging markets of China, India and Malaysia, including PetroChina/CNP, China Petroleum & Chemical Corporation/Sinopec, ONGC and PETRONAS via two publicly listed subsidiaries.

In addition to advocating for genocide-free investing on humanitarian and legal grounds, IAG believes that it is consistent with the objectives and spirit of the US economic sanctions (now lifted) in Sudan and stated values and commitments of investment firms. A further strong argument in favor of the resolution made by IAG is that there is broad-based support for genocide-free investing, as validated according to research conducted by KRC (a unit of the publicly traded Interpublic Group of Companies (IPG)) in 2007 and 2010 showing that 88% of respondents want their mutual funds to be genocide-free. Recent shareholder proposals and proxy votes that have earned strong shareholder endorsements along with actions by firms such as T. Rowe Price and TIAA-CREF to implement policies on investments tied to genocide also offer support for IAG’s position.

Five Companies Have Been Identified: China Petroleum & Chemical Corporation (SINOPEC). PetroChina Company Limited, Oil and Natural Gas Corporation Limited (ONGC) and Petroliam Nasional Berhad (PETRONAS), Including Petronas Chemicals and Petronas Gas Berhad

The companies listed below have been identified by Investors Against Genocide for their operations in Sudan and significant business partnerships with the Government of Sudan. These are listed companies, in part or in whole, with stocks that trade in local markets and in some cases in the form of ADRs listed for trading on NYSE. These firms have also issued bonds. Their stocks and bonds are most likely to be held in actively managed equity and bond funds as well as index funds with a global mandate that includes developing markets, emerging markets and Asia-Pacific region, in particular, as well as global bond funds. For example, the stock of all five companies was held in the Vanguard Emerging Markets Stock Index Fund as of September 30, 2017.

China Petroleum & Chemical Corporation (SINOPEC). A subsidiary of China Petrochemical Corporation, Beijing-based SINOPEC is an energy and chemicals company engaged in oil, gas and chemicals operations, including the exploration for and development of oil fields, production and sales of crude oil and natural gas, to mention just a few of its operations.

SINOPEC is the third-largest company of China by revenue, recording $255.7 billion in sales and assets in the amount of $216.7 billion. SINOPEC is listed in Hong Kong and also trades in Shanghai and New York on the NYSE in the form of ADRs (NYSE: SNP).

PetroChina Company Limited. A Chinese oil and gas company engaged in a range of activities that include the refining, exploration, development, production, marketing of crude oil and

natural gas as well as transmission and sale of natural gas, crude oil, and refined products. The company operates as a subsidiary of state-owned China National Petroleum Corporation, headquartered in Dongcheng District, Beijing. PetroChina is China’s biggest oil producer and the world’s fourth-largest oil and gas company by revenues, generating $214.8 billion in sales with assets in the amount of 344.9 billion. PetroChina Company Limited ADRs are listed on the NYSE (NYSE: PTR).

Oil and Natural Gas Corporation Limited (ONGC). An India-based publicly listed global energy holding company whose shares are largely owned by the Government of India (68.94%) with the remaining shares held by institutional and retail investors. Its $19.9 billion in revenue and $57.7 billion in assets sourced to the company’s activities in the exploration, development and production of crude oil and natural gas within and outside India. It is the largest crude oil and natural gas producer in India.

Petroliam Nasional Berhad (PETRONAS). PETRONAS is Malaysia’s fully integrated oil and gas multinational that is largely owned by the Malaysian Government. The firm’s business activities include but are not limited to the exploration, development and production of crude oil and natural gas in Malaysia and overseas, the liquefaction, sale and transportation of Liquefied Natural Gas (LNG), the processing and transmission of natural gas and the sale of natural gas products and the refining and marketing of petroleum products.

While PETRONAS is privately held, two of its subsidiary companies, both majority owned by PETRONAS, Petronas Chemicals (PGC), which generated $3.3 billion in revenues and reported assets of $14 billion, and Petronas Gas Berhad (PGB), with revenues of $1.1 billion and assets in the amount of $8.8 billion, are listed for trading on the Malaysian Stock Exchange. PETRONAS owns 64.35% of PGC and 60.63% of PGB while the remaining 35.6% and 39.37% are held by financial institutions and retail shareholders.

Interestingly, both publicly listed firms are constituent members of the FTSE4Good Bursa Malaysia Index which is designed to highlight companies that demonstrate a leading approach to addressing environmental, social and governance risks[4].

Vanguard Opposes the Genocide-Free Investing Resolution for Various Reasons

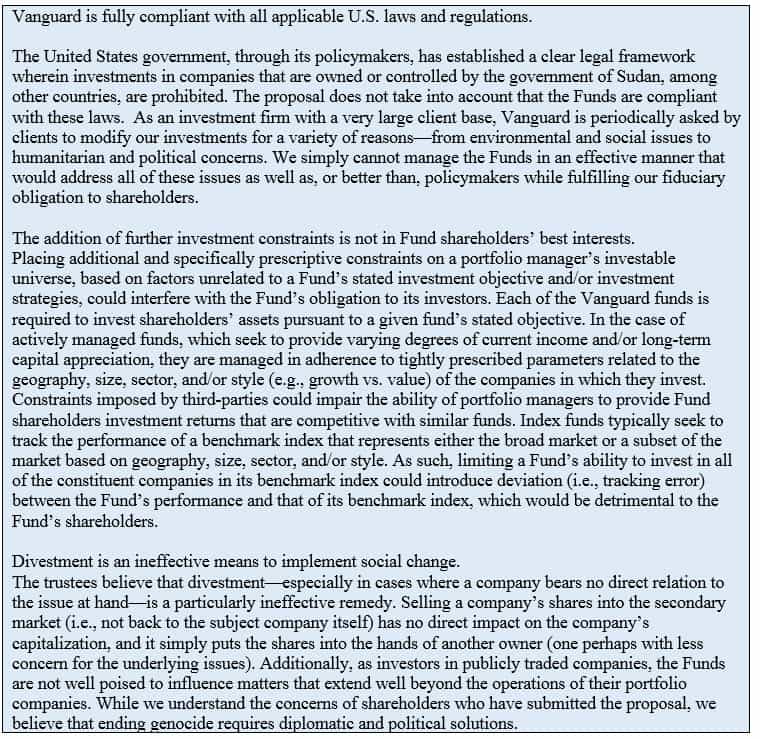

The trustees of the named Vanguard funds recommend that shareholders vote against this proposal. According to Vanguard’s detailed response, the humanitarian issues on which this proposal is ultimately focused are of consequence and deep concern. At the same time, meaningful long-term solutions to these issues require diplomatic and political resources to come together to implement change. Vanguard notes that its funds are compliant with all applicable US laws on this matter. In addition, the proposal would interfere with the advisors’ fiduciary duty to manage funds in line with their investment objectives and strategies. Finally, Vanguard adds that it believes that the divestment contemplated by the proposal would be an ineffective means to implement the social change it seeks. Refer to Vanguard’s detailed response in the accompanying box.

Vanguard’s Detailed Response to IAG’s Resolution

Investment Options for Concerned Genocide-Free Investors

Should the resolution be rejected by Vanguard’s shareholders as expected, investors concerned about the possibility of inadvertently investing in any of the companies noted above can conduct their own due diligence research into the securities holdings of funds that are most likely to hold shares or bonds in any of the identified firms and/or have the flexibility to invest in such firms currently or in the future[5]. Although securities listed and traded in the US in the form of ADRs could technically be included in US-focused funds, this not probable. Rather, these securities are most likely to be held in actively managed equity and bond funds as well as index funds with a global mandate that include developing markets, emerging and Asia-Pacific focused markets, in particular, as well as global bond funds.

More generally, however, investors who wish to implement a genocide-free investment strategy should consider the option of pivoting to mutual funds that explicitly integrate environmental, social and governance factors into their investment strategy and decision making. Rather than relying exclusively on strategies based on negative screens, such firms employ industry and company-specific positive selection criteria to identify potentially positive investment opportunities or achieve risk reduction. Such a strategy may also encapsulate shareholder advocacy and active proxy voting. Funds in this category, even in the absence of specific exclusionary criteria for genocide or related controversies, are more likely to exclude firms engaged in genocide for governance and social reasons and also to limit exposure to fossil fuel companies due to environmental concerns.

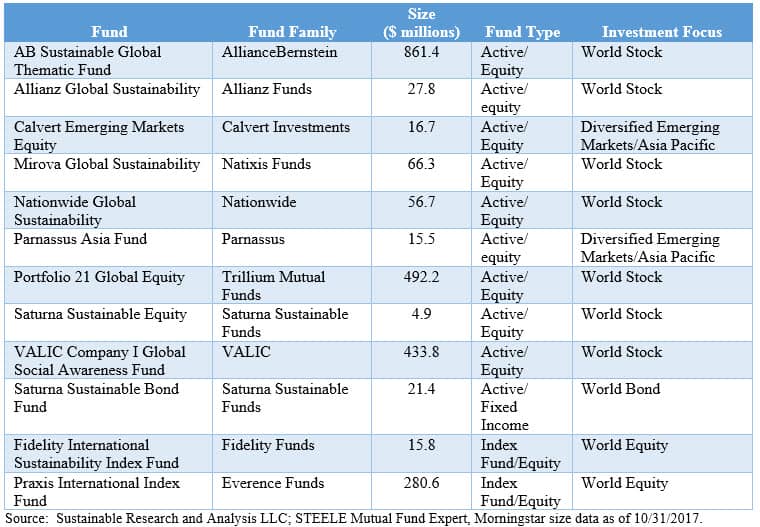

The accompanying Table 1 reflects the results of screening and analysis conducted for the purpose of identifying actively managed funds and index funds pursuing a global mandate that includes developing markets, emerging markets and the Asia-Pacific region, in particular, as well as global bond funds. Excluded from the list are thematic funds, or funds that focus strictly on environmental issues, alternative energy, low-carbon strategies funds that invest strictly in green bonds as well as funds whose prospectus benchmark is inconsistent with a strategy of investing in developing markets, emerging markets and the Asia-Pacific region. The listing of funds has been compiled by focusing strictly on funds that employ company-specific positive ESG selection criteria that may be combined with company engagement and active proxy voting practices rather than funds that have implemented broad-based negative screens in assessing ESG practices. The list, therefore, is more restricted as it also excludes faith-based funds, or funds that screen and exclude investments based largely on one or more exclusionary practices. Further, the list does not include ETFs that may offer concerned investors yet another option.

Table 1: ESG Funds with Global Investment Mandates, Including Developing Markets, Emerging Markets and Asia-Pacific Region (Listed in Alphabetical Order within Fund Type)

In a future article, these funds will be more formally evaluated along with ETF options. In the meantime, investors should be cautioned that, as is the case before investing in funds more generally, due diligence should be conducted to ensure that, at minimum, these funds satisfy basic requirements, including qualifications and skills to combine financial and sustainability characteristics, a demonstrated, established and consistent performance track record over time, and properly sized for scale and liquidity and effectively priced fund offerings. In any case, investors have to be clear about their sustainability objectives to ensure that these are properly aligned with their portfolio profiles.

[1] The Vanguard FTSE Social Index Fund.

[2] ETFs offer investors another option and this will be covered in a subsequent article.

[3] Executive Order 13400 as of April 26, 2006, as reported in the Federal Register, Vol. 71, No. 83.

[4] Both PGC and PGB are constituent member companies of the index as of 10/31/2017.

[5] Fund holdings are posted on Vanguard’s website along with fund prospectuses.