Sustainable Bottom Line: In addition to lacking a common definition of “impact,” fund level impact reporting by funds with “impact” in their name is limited.

Sustainable funds that refer to “impact” in their names reflect variations in the definition of impact while at the same time, reporting and disclosure practices vary

Of 533 labeled sustainable long‐term mutual funds (share classes collapsed) and ETFs as of April 2026, about 338 funds reflect a sustainable reference in their name. These include 128 funds that carry “sustainable” or “sustainability” in their name, 96 reference “ESG,” 26 use “impact,” 19 invoke “climate,” and 13 each cite “responsible investing” or “green.” Smaller cohorts that add up to a total of 43 additional funds reference clean energy or clean tech, carbon, environment, water, transition, and SDG (UN’s Sustainable Development Goals). More specifically regarding the funds that refer to the term “impact” in their names, the 26 identified funds are almost equally divided between bond funds, both taxable and municipal funds, as well as equity funds, domestic as well as international funds. These investment vehicles are dominated by actively managed funds, but four index funds are also offered. In addition, these funds reflect variations in their definitions of impact as well as their reporting and disclosure practices. As for the definition of “impact,” there is no industry-standard definition of “impact” and definitions range from narrow (use-of-proceeds for bonds) to broad (ESG integration + values). Interestingly, there is a bond vs. equity divergence. Bond funds predominantly use use-of-proceeds frameworks (International Capital Markets Associations (ICMA) Green/Social Bond Principles) while equity funds more commonly reference SDGs, ESG integration strategies, or proprietary frameworks. Definitional variations may narrow following the implementation of the SEC’s amended Name Rules that goes into effect in June 2026. Refer to Sustainable funds meet the Names Rule: What to watch for as the June deadline lands*. https://sustainableinvest.com/sustainable-funds-meet-the-names-rule-what-to-watch-for-as-the-june-deadline-lands/. Sustainable investors contemplating investments in one or more of the 26 “impact” named funds, in particular, who are more likely to place greater emphasis on the achievement of positive social and/or environmental outcomes relative to the achievement of market-rate financial returns, are also more likely to seek funds that offer more rigorous impact disclosure and reporting.

Review and analysis of impact reporting and disclosure practices conducted along two dimensions show significant variations in rigor

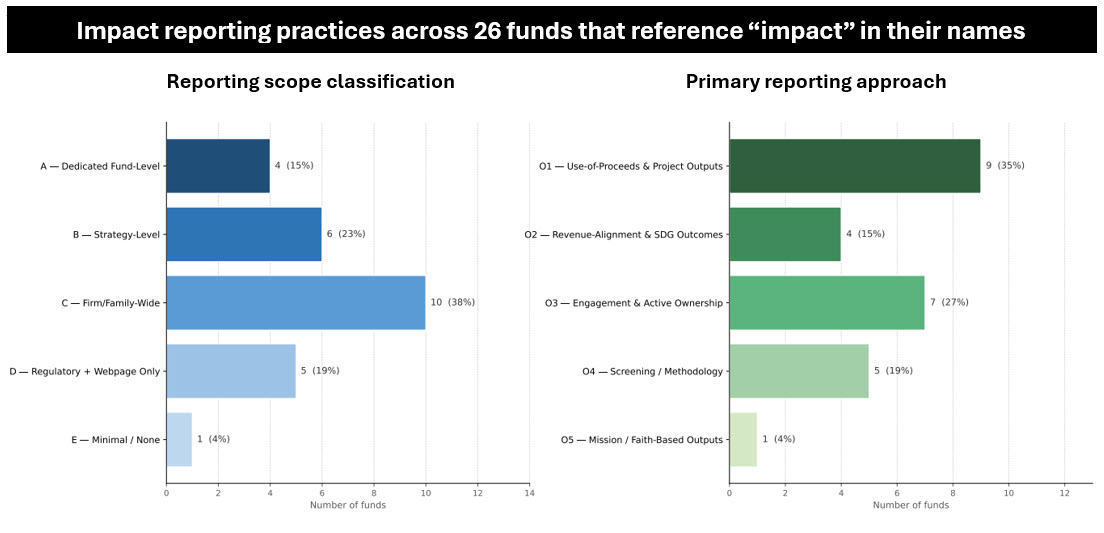

A review and analysis of the impact reporting and disclosure practices of the 26 named “impact” funds was conducted along two dimensions. The first is reporting scope, capturing the character of the impact disclosure coverage hierarchy, for example, fund level, strategy level, firm-wide level, etc. The second dimension refers to the primary reporting approach, or how impact is reported. Some funds have a secondary approach where two approaches are equally prominent. The overall picture is one of significant variations in rigor.

Notes of Explanation: Data as of April 30, 2026. Refer to definitions of terms. Sources: Sustainable Research and Analysis LLC. and Morningstar.

Reporting scope: 14 of 26 funds publish a dedicated impact report but their scope varies

The research indicates that 14 of the 26 funds publish a dedicated impact report (54%), eleven are covered indirectly via firm-level or strategy-level disclosures (42%), and only one, the Payden California Municipal Social Impact, has essentially no impact-specific reporting beyond its fact sheet (4%). By scope, firm- or family-wide reports dominate (10 funds, 38%), followed by strategy-level (6, 23%), regulatory plus webpage only (5, 19%), dedicated fund-level (4, 15%), and minimal or none (1, 4%). The four dedicated fund-level reports are published by T. Rowe Price Global Impact Equity, Hartford Global Impact (via Wellington), RBC BlueBay Impact Bond, and Nia Impact Solutions.

Reporting approach: Use-of-proceeds and project outputs are the most common characteristics

By primary reporting approach, use-of-proceeds and project outputs is the most common (9 funds, 35%) characteristic of bond and municipal funds reporting affordable housing units, megawatts of renewable energy, jobs supported, and similar project-level metrics. Engagement and active ownership (7, 27%) is the dominant approach for equity-focused managers including Boston Common, Domini, and UBS, who report dialogues, shareholder proposals, and proxy votes. Screening and methodology disclosure (5, 19%) characterizes the two Impact Shares ETFs, American Century MID, and the recently launched Praxis ETFs, which describe what they exclude rather than what they have achieved. Only four funds (15%) report through revenue-alignment and aggregated SDG outcomes, the most quantitative approach available to equity funds, and a single fund (GuideStone, 4%) reports primarily through mission and faith-based outputs.

*Note: Subsequent to the publication date of this article, the number of funds that reflect a sustainable reference in their names was updated to 338 from 343.

A listing of the 26 “impact” funds along with their reporting practices is provided below.

Listing of "impact" funds and their reporting practices

| Fund Name | Asset Class / Style | Reporting Scope | Primary Approach | Secondary Approach |

| AB Impact Municipal Income | US Municipal Bond | B | O1 | |

| AMG Boston Common Global Impact | Global Equity | C | O3 | O2 |

| American Century Mid Cap Gr Impact ETF | US Mid-Cap Growth Equity | D | O4 | O2 |

| Boston Common ESG Impact Em Mkts | Emerging Markets Equity | C | O3 | O2 |

| Boston Common ESG Impact Intl | International Developed Equity | C | O3 | O2 |

| Boston Common ESG Impact US Equity | US Large-Blend Equity | C | O3 | O2 |

| CCM Community Impact Bond | US Investment-Grade Bond (Community Development) | B | O1 | |

| Domini Impact Bond | US Investment-Grade Intermediate Bond | C | O1 | O3 |

| Domini Impact Equity | US Large/Mid-Cap Equity | C | O3 | O4 |

| Domini Impact International Equity | International Developed Equity | C | O3 | O4 |

| GuideStone Funds Impact Bond | Global Fixed Income (Faith-Based) | B | O5 | O1 |

| Hartford Global Impact | Global Equity | A | O2 | O3 |

| Impact Shares NAACP Minority Empwrmt ETF | US Large/Mid-Cap Equity (Index) | D | O4 | |

| Impact Shares Women’s Empowerment ETF | US Large/Mid-Cap Equity (Index) | D | O4 | |

| Neuberger Municipal Impact | US Municipal Bond | D | O1 | |

| Nia Impact Solutions | Global Large-Cap Equity | A | O2 | O4 |

| Nuveen Core Impact Bd Mngd Accnts Common | US Investment-Grade Core Bond (Managed Account) | B | O1 | |

| Nuveen Core Impact Bond | US Investment-Grade Core Bond | B | O1 | |

| Nuveen Short Duration Impact Bd | US Investment-Grade Short-Duration Bond | B | O1 | |

| Payden California Municipal Scl Imp | California Municipal Bond | E | O1 | |

| Praxis Impact Bond | US Investment-Grade Intermediate Bond (Faith-Based) | C | O1 | O3 |

| Praxis Impact Large Cap Growth ETF | US Large-Cap Growth Equity (Faith-Based) | C | O4 | O3 |

| Praxis Impact Large Cap Value ETF | US Large-Cap Value Equity (Faith-Based) | C | O4 | O3 |

| RBC BlueBay Impact Bond | US Investment-Grade Bond | A | O2 | O1 |

| T. Rowe Price Global Impact Equity | Global Equity | A | O2 | O3 |

| UBS Engage For Impact | Global Equity | D | O3 | O2 |

Reporting Scope Classification

Code Label Definition

A. Dedicated Fund-Level Impact Report. A fund-specific impact report (PDF or web), with metrics tied to this particular fund/strategy.

B. Strategy-Level Impact Report. Single impact report covering the underlying strategy across share classes or wrappers (mutual fund + SMA, etc.).

C. Firm- or Family-Wide Impact Report. One impact report covers many funds in the family or the manager’s full impact platform.

D. Regulatory + Webpage Disclosures. Only No dedicated impact report; impact disclosure limited to SEC shareholder reports (N-CSR), fund pages, factsheets, and firm-level sustainability materials.

E. Minimal / No Dedicated Impact Reporting. Essentially no impact-specific disclosure beyond a strategy summary; factsheet and prospectus only.

Primary / Secondary Reporting Approach

Code Label Definition

O1. Use-of-Proceeds & Project Outputs. Typical of bond/municipal funds: reports project-level outputs financed (affordable housing units, MW renewable, students served, gallons treated, jobs supported).

O2. Revenue-Alignment & SDG Outcomes. Typical of impact equity funds: % of holdings/revenue aligned to impact themes/SDGs, plus aggregated company-level outcome KPIs (tCO2 avoided, patients treated, etc.).

O3. Engagement & Active Ownership. Reports number of dialogues, shareholder proposals, proxy votes, milestones achieved on ESG/impact themes.

O4. Screening / Methodology Disclosure. Index-based or rules-based: discloses screening criteria, exclusions, and index methodology rather than realized outcomes.

O5. Mission / Faith-Based Outputs. Faith- or mission-aligned outputs: donations to ministries, beneficiaries served, denominational impact narratives.