Sustainable Bottom Line: May 2026 returns by top 10 fund performers, up 21.5% and powered by three overlapping themes, are not likely to be repeated.

Notes of Explanation: Funds listed in descending order based on their total return performance in May 2026. In the case of mutual funds with multiple share classes, only the best performing share class is listed. Sources: Morningstar and Sustainable Research and Analysis LLC.

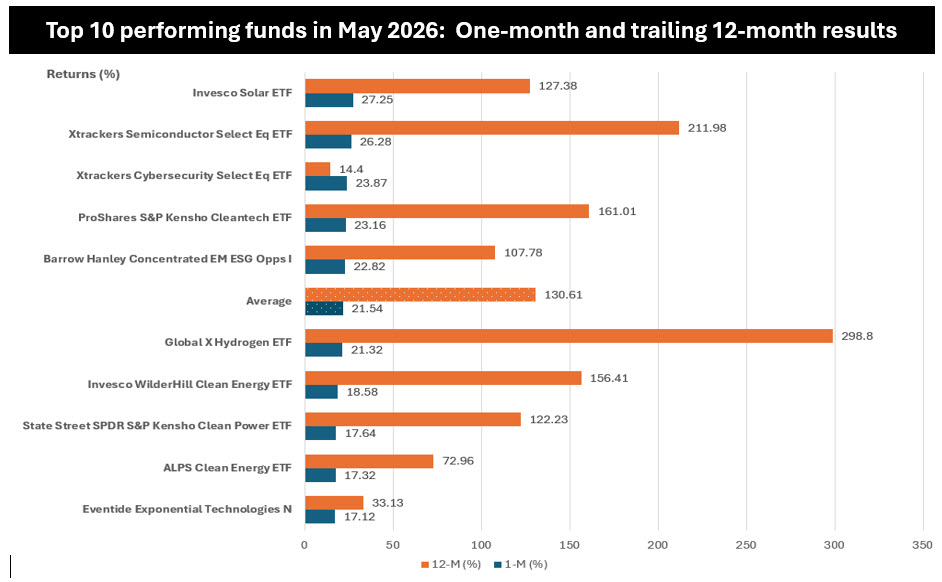

Observations:

• U.S. equity markets capped an exceptional month with all three major indexes closing at record highs on the final trading day of May. The technology-laden Nasdaq-100 Index led the advance, posting a gain of 10.6% for the month and a year-to-date gain of 20.45% while the S&P 500 rose 5.3% and 11.3% over the same periods. Labeled sustainable long-term funds added an average of 3.2% in May and 23.6% over the trailing 12-months. At the same time, the ten best performing labeled sustainable funds, of which four incorporate explicit ESG criteria in stock selection, recorded an average increase of 21.5% and an eye-popping average of 130.6% since June 2025. Looking across the group that includes eight index tracking and two actively managed funds, three overlapping themes explain the bulk of the returns, applicable to seven of the ten funds. Repeating 21.5% in a single month, or 130% over the next twelve months, is not a realistic expectation for this group in the aggregate.

• The AI-power nexus and clean energy’s rehabilitation. The largest single driver was the intersection of artificial intelligence infrastructure buildout and clean energy demand, based on surging demand and capacity projections. Solar funds, Invesco Solar ETF (TAN), up 27.25%, ProShares S&P Kensho Cleantech ETF (CTEX), up 23.16%, Invesco WilderHill Clean Energy ETF (PBW), up 18.58%, State Street SPDR S&P Kensho Clean Power ETF (CNRG), up 17.64%, and ALPS Clean Energy ETF (ACES), up 17.32%, all benefited from this structural demand story. But there is a second, equally important force. These funds entered 2025 pricing in severe Inflation Reduction Act (IRA) rollbacks that proved far less damaging than feared. That combination, deep pessimism lifting against a backdrop of genuine demand growth, produced the multi-hundred percent trailing 12-month gains for the solar and cleantech group. It should be noted that five of the ten funds in operation over the previous five years are still recovering from steep declines sustained between 2022 -2024 before this recovery.

• Semiconductors and the agentic AI wave. The Xtrackers Semiconductor Select Equity ETF (CHPS) led the group on a trailing 12-month basis at +211.98%, with a May return of +26.28%. Broadcom’s AI revenue more than doubled, up 106%, on demand for custom accelerators and networking chips, while AMD data center revenue grew 57% in Q1 2026. The shift from generative AI toward agentic AI applications is driving a new round of capacity investment, and chip demand continues to outpace supply. May’s strong month was amplified by the US-China trade truce announced mid-month, which directly benefited semiconductor stocks exposed to Asian supply chains and end markets.

• Cybersecurity’s structural compounding. The Xtrackers Cybersecurity Select Equity ETF (PSWD), up 23.87% in May, has a significantly lower 12-month return of only 14.4% compared to its peers in the top 10 list, signaling that this fund’s May surge reflects more recent acceleration rather than a multi-year recovery trade. AI-driven expansion of attack surfaces, cloud migration, and geopolitical tensions are producing structural, recurring demand for security platforms. Top holdings, CrowdStrike, Palo Alto Networks, Fortinet, and Zscaler, are seeing sustained enterprise budget prioritization. This is a fundamentally different risk profile than the clean energy names: less mean-reversion, more durable revenue growth.

• Hydrogen’s spectacular, structurally complicated comeback. Global X Hydrogen ETF (HYDR) posted the highest trailing 12-month return in the group at +298.8%, recovering from extreme lows driven by years of investor abandonment, project delays, and policy uncertainty. Near-term catalysts include Plug Power contract wins and Air Products’ NEOM Green Hydrogen Project (90% complete, targeting 2027 production). However, the structural picture is sobering. Cummins, Inc., a global technology company, has stated that demand for green hydrogen has “dried up, dramatically lower,” 40 projects revised their 2026 timelines, and the Trump administration cut $3 billion in hydrogen funding. The 298% trailing 12-month gain is a recovery-from-the-abyss story and may represent a demand-driven fundamental rerating.

• Emerging markets value-ESG. The smallish $11 million net assets actively managed Barrow Hanley Concentrated Emerging Markets ESG Opportunities I (BEOIX) that was launched just short of three years ago, up 22.82% in May and 107.78% over the trailing 12-months, benefited from Korea and Taiwan outperformance driven by surging memory chip prices and strong earnings, alongside a broader EM recovery as tariff fears moderated in May. Barrow Hanley’s concentrated, value-oriented approach in EM appears to have captured country and sector exposures, particularly technology hardware, that amplified these trends.

• Exponential Technologies. Eventide Exponential Technologies N (ETNEX), up 17.12% in May and 33.13% over the trailing twelve months, is another outlier in terms of its twelve month return, more modest than its top 10 peers, but its May return reflects broad participation in the AI/technology rally. Its holdings span technology enablers across sectors aligned with Eventide’s values-based screening approach.

• Only four of 10 funds incorporate explicit ESG criteria in stock selection, and they do so in meaningfully different ways. Both index CHPS and PSWD ETFs use Sustainalytics to apply hard exclusionary screens to their sector universes before index construction: UN Global Compact compliance, an ESG risk score below 40, no controversial weapons, no tobacco/assault weapons, and revenue thresholds from fossil fuels and other excluded sectors. Notably, these two funds apply ESG screening to non-clean-energy sectors (semiconductors and cybersecurity), which is the opposite of the other eight funds. BEOIX offers the most rigorous ESG integration of the group. An active fund combining exclusionary screens (tobacco, fossil fuels, controversial weapons, alcohol/gambling/pornography, human rights violators) with full ESG materiality analysis embedded in bottom-up fundamental valuation, using proprietary materiality mapping, internal ESG scores, and third-party data. Finally, ETNEX, the only other actively managed fund, uses a faith-informed Business 360 values framework (about 50 ethical criteria covering human dignity, weapons, community, governance, and environmental stewardship) integrated into fundamental stock selection. It draws on Christian values rather than institutional ESG frameworks. The other 7 funds, TAN, CTEX, HYDR, PBW, CNRG, ACES, and SPDR CNRG, are labeled sustainable purely on thematic grounds (solar, cleantech, hydrogen, clean power, clean energy). Their index methodologies contain no ESG screens on individual company practices.