Sustainable Bottom Line: Investors will benefit from greater transparency with improved definitions and disclosure of the criteria applied in the implementation of its sustainable approaches.

SEC amended Names Rule goes into effect next month

The SEC’s amended Names Rule (Rule 35d‑1) takes a meaningful step forward on June 11, 2026. At that time, now less than a month away, fund groups with more than $1 billion in net assets must comply with the expanded 80% investment policy under the SEC’s amended Names Rule. For funds whose names suggest sustainability, ESG, impact, climate, green, or a related focus, this is not minor housekeeping. It is a compliance test with publication‐ready consequences for prospectuses, statements of additional information, marketing materials, and Form N‐PORT filings. Some funds may already be complying while others have taken actions to eliminate the obligation to comply by deleting named references. But this is not the case for all the 343 or so funds out of 533 labeled sustainable funds, or 64%, that reflect a sustainable reference in their name according to research conducted by Sustainable Research and Analysis (SRA). Following the completion of the 24-month implementation cycle, investors will benefit from greater transparency and disclosure as the covered subset of labeled sustainable mutual funds and ETFs take steps to define their sustainable terms and refine their taxonomies, methodologies, as well as criteria used in the implementation of their investing approaches, in line with the amended Names Rule. The amended Names Rule will help address some but certainly not all of the concerns that arose around ESG-related terms in the investment fund space, as well as evolving investor expectations around terms such as “sustainable” or “socially responsible” that have led to investor confusion and misunderstanding while compounding the potential for greenwashing in fund names.

As many as 343 sustainable funds offered by about 82 investment management firms may be subject to the amended Names Rule

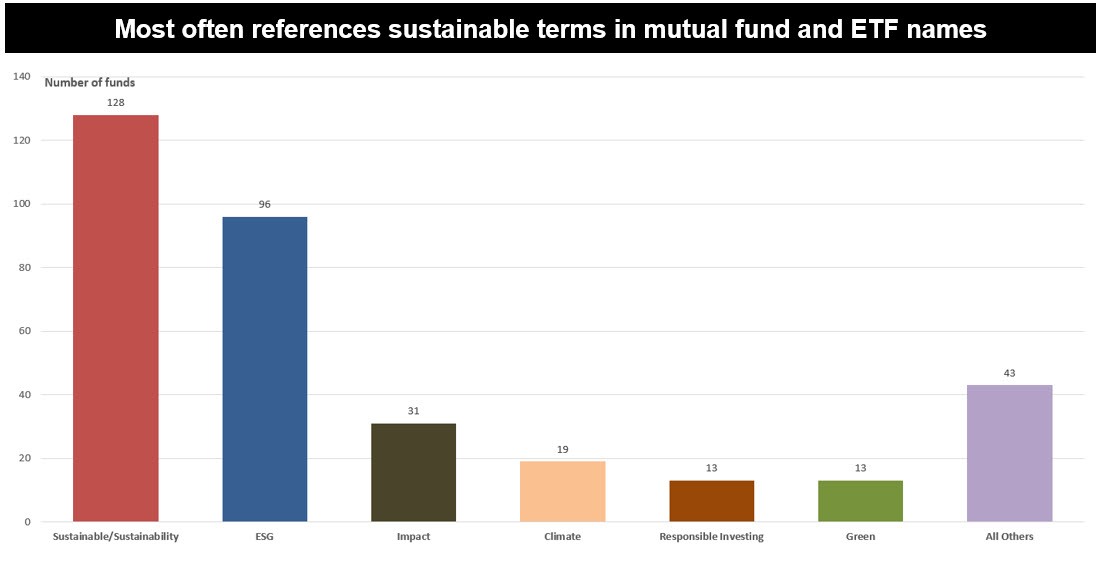

A name‐level analysis of 533 labeled sustainable long‐term mutual funds (share classes collapsed) and ETFs, illustrates the scale. There are about 343 funds that reflect a sustainable reference in their name. Of these, 128 carry “sustainable” or “sustainability” in their name, 96 reference “ESG,” 31 use “impact,” 19 invoke “climate,” and 13 each cite “responsible investing” or “green.” Smaller cohorts reference clean energy or clean tech, carbon, environment, water, transition, and the UN’s SDGs. The 343 funds span 86 fund firms, and about 82 of these firms have company‐wide assets under management (AUM) at or above $1 billion. That said, the segment is highly concentrated with the largest 15 or so firms accounting for about 70% of the funds subject to the amended Names Rule.

Notes of Explanation: Data as of April 30, 2026. Total number of labeled sustainable long-term funds = 533 funds (share classes have been collapsed). Responsible investing and green are tied with 13 funds each. All others includes: Clean Energy/Carbon (9), Carbon (9), Environment (9), Water (7), Transition (6) and SDG (3). Sources: Sustainable Research and Analysis LLC and Morningstar.

Broad requirements under the amended Names Rule

Under the amended rule, any fund whose name uses a term suggesting an investment focus, theme, or characteristic, and that explicitly includes ESG and sustainability terms, must adopt and apply a policy to invest at least 80% of its assets consistent with that name. The fund must define the terms used in its name reasonably, reflecting their plain‐English meaning or established industry use, and disclose those definitions in the prospectus. The related Form N‐PORT reporting that would identify which holdings count toward the 80% test was further extended by the SEC in February 2026 to November 17, 2027 for fund groups above $10 billion in net assets and May 18, 2028 for fund firms with assets below that level, but the substantive 80% policy obligation still arrives in June for groups with assets above $1 billion.

What investors and advisors should watch

Prospectus definitions. Updated risk and strategy sections will reveal how each fund defines “sustainable,” “ESG,” “impact,” or “climate.” Vague language such as “we consider ESG factors” is unlikely to suffice. Look for explicit definitions, the data sources or scoring methodologies used, the share of the portfolio that qualifies, and how the 80% test is computed and rebalanced.

Name changes and relabeling. Expect some funds to rename in order to avoid the 80% obligation, dropping “sustainable” or “ESG” if the manager cannot demonstrate that holdings meet the test or may not wish to do so for various reasons. Funds that keep their labels signal conviction and accept the discipline that comes with it. Both moves carry information value for investors and financial intermediaries. One recent example involves the Neuberger Quality Equity Fund that recently dropped the term “sustainable” from its name but preserved its sustainable investing criteria as part of the fund’s principle investment strategy.

Methodology shifts. To comply, funds may tighten screens, or they may elect to change index providers, or adjust benchmarks. These can quietly alter sector exposures, tracking error, and performance characteristics in ways that are not obvious from marketing materials. Investors and others should read the supplemental prospectus filings (485APOS, 497) with care.

Regulatory crosscurrents. SEC Chair Paul Atkins indicated in February 2026 that the 2023 amendment is under review with an eye toward reducing reporting burdens, and staff have since issued clarifying FAQs. Further modifications, or selective non‐enforcement positions, remain possible, particularly for the more contested ESG‐specific provisions.

For advisors, the practical step is to inventory client holdings against this term list, flag funds expected to refile or rename and prepare clients for the possibility that what they own may carry a different label, a tighter screen, or a refined strategy by year‐end. The largest fund families offering funds with names that must qualify under the Names Rule, such as BlackRock/iShares, Vanguard, Fidelity, State Street and JP Morgan, to name just five that collectively account for about 50% of the sustainable‐labeled product on the market, and their responses will likely set the tone for the rest of the industry. Sustainable‐labeled funds are about to become more transparent, more defined, and in some cases more selective about who keeps the label.

Here is how the amendments impact ESG, sustainable, climate, impact funds, etc. more specifically:

1. ESG/sustainable/climate/impact names are squarely in scope. The original 2001 rule covered names suggesting a focus on a type of investment, industry, country, or geographic region. The 2023 amendments expanded coverage to names suggesting investments with "particular characteristics," and the adopting release expressly identified ESG, sustainability, and similar terms as triggering the rule. A fund called "XYZ Sustainable Equity Fund" or "ABC Climate Solutions Fund" must now adopt a policy to invest at least 80% of its assets in investments that fit the characteristic the name suggests. The same applies to "impact," "green," and "socially responsible."

2. "Integration" funds face a real naming decision. This is the most consequential operational issue for the sustainable space. Under prior staff guidance, funds that merely "integrated" ESG factors alongside many others were distinguished from funds where ESG was a determinative or significant factor. The amended rule and the adopting release commentary together make clear that a fund using ESG-suggestive terminology in its name must treat ESG as more than one factor among many — assets must actually be selected for those characteristics. Pure "integration" funds will likely need to rebrand or materially change their selection process, which is a real disruption given how many U.S. funds adopted "ESG integration" language during the 2018–2022 wave.

3. Funds must define their terms and the definition must be "reasonable." The rule does not define "sustainable," "ESG," "climate," or "impact," and the SEC declined to impose definitions. But the adopting release requires that a fund use the term in a way consistent with its plain-English meaning or established industry use, and the prospectus must disclose the criteria the fund applies. This is where greenwashing enforcement risk concentrates: a fund whose 80% bucket is populated by holdings whose ESG/climate credentials don't withstand scrutiny is exposed under both the Names Rule and the anti-fraud provisions. Expect Investment Management exam staff to ask, at minimum, what the taxonomy is, how it's applied, who applies it, and how exceptions are documented.

4. "Impact" is the trickiest of the four terms. For ESG, sustainable, and climate, an asset-level characteristic test is workable, even if subjective. "Impact" is harder because the canonical definition (additionality, intentionality, measurement) is investor-action-oriented rather than asset-attribute-oriented. The SEC didn't address this neatly in 2023, and the February 2026 FAQs did not resolve it. Funds with "impact" in the name should expect questions about how a public-equity portfolio satisfies an 80% test under an "impact" characterization, and many advisers may move toward terms like "thematic" or "solutions" that map more comfortably onto an 80% policy.

5. Quarterly testing replaces point-of-purchase testing. The amendments require quarterly compliance assessment, and funds that fall out of compliance for reasons other than market movement must come back into compliance "as soon as reasonably practicable,” generally within 90 days. For a sustainable/climate fund, a portfolio that drifts because a holding becomes less "sustainable" by the fund's own taxonomy (e.g., an issuer's behavior change or a downgrade by a data provider) may require active remediation, not just a passive wait. This bites harder for thematic strategies with concentrated baskets.

6. Notice requirements and recordkeeping. Funds must adopt the 80% policy as either fundamental or non-fundamental (with 60 days' notice required for changes) and must keep records evidencing 80% determinations for the long haul. The February 2026 FAQs offered modest relief here, clarifying that minor compliance-driven tweaks to a non-fundamental 80% policy don't trigger the 60-day notice, useful for advisers refining their taxonomy as data and methodologies evolve.

7. What you're likely to see in the market. Several waves are already visible. The "soft rebrand" wave where funds quietly dropping ESG/sustainable/climate language from names they consider hard to defend — has been ongoing since 2023 and Morningstar has documented steady decline in U.S. sustainable fund name counts. The "tighten the taxonomy" wave involves funds doubling down on the name but publishing more rigorous criteria and adding third-party screens. The "merge or close" wave is concentrated in smaller funds where compliance cost exceeds AUM economics. And in multi-strategy fund families, you're seeing strategy bifurcation, with an explicit ESG sleeve separated from a general sleeve so the parent fund's name doesn't carry the 80% obligation.

8. The wild card is the Atkins-era SEC. The unusual feature of this moment is the regulatory uncertainty. The 80% requirement is still scheduled to go live June 11 for the largest fund groups, but the Commission is publicly reviewing the rule, has withdrawn the related Biden-era ESG disclosure proposals, extended the N-PORT reporting components, and issued FAQs that soften certain edges. Most counsel are advising sustainable fund sponsors to assume June 11 will hold (no further extension has been announced for the underlying 80% policy itself), while being ready for further staff guidance or even a more substantive rollback. Enforcement priorities under Atkins also suggest a less aggressive posture on standalone greenwashing-style cases, though Names Rule enforcement through the antifraud lens remains squarely on the table.